前言

- 💖💖作者:计算机程序员小杨

- 💙💙个人简介:我是一名计算机相关专业的从业者,擅长Java、微信小程序、Python、Golang、安卓Android等多个IT方向。会做一些项目定制化开发、代码讲解、答辩教学、文档编写、也懂一些降重方面的技巧。热爱技术,喜欢钻研新工具和框架,也乐于通过代码解决实际问题,大家有技术代码这一块的问题可以问我!

- 💛💛想说的话:感谢大家的关注与支持!

- 💕💕文末获取源码联系 计算机程序员小杨

- 💜💜

- 网站实战项目

- 安卓/小程序实战项目

- 大数据实战项目

- 深度学习实战项目

- 计算机毕业设计选题

- 💜💜

一.开发工具简介

- 大数据框架:Hadoop+Spark(本次没用Hive,支持定制)

- 开发语言:Python+Java(两个版本都支持)

- 后端框架:Django+Spring Boot(Spring+SpringMVC+Mybatis)(两个版本都支持)

- 前端:Vue+ElementUI+Echarts+HTML+CSS+JavaScript+jQuery

- 详细技术点:Hadoop、HDFS、Spark、Spark SQL、Pandas、NumPy

- 数据库:MySQL

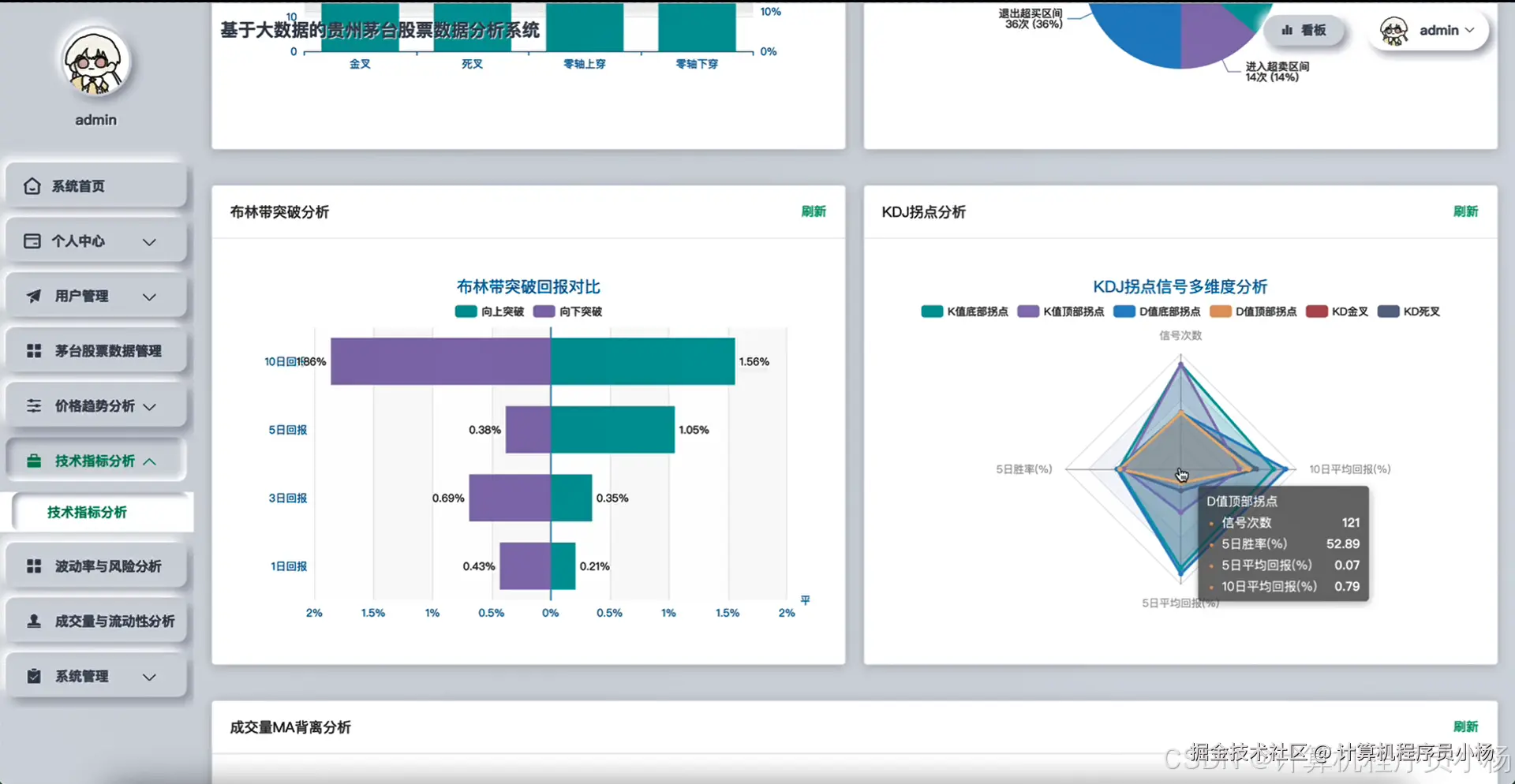

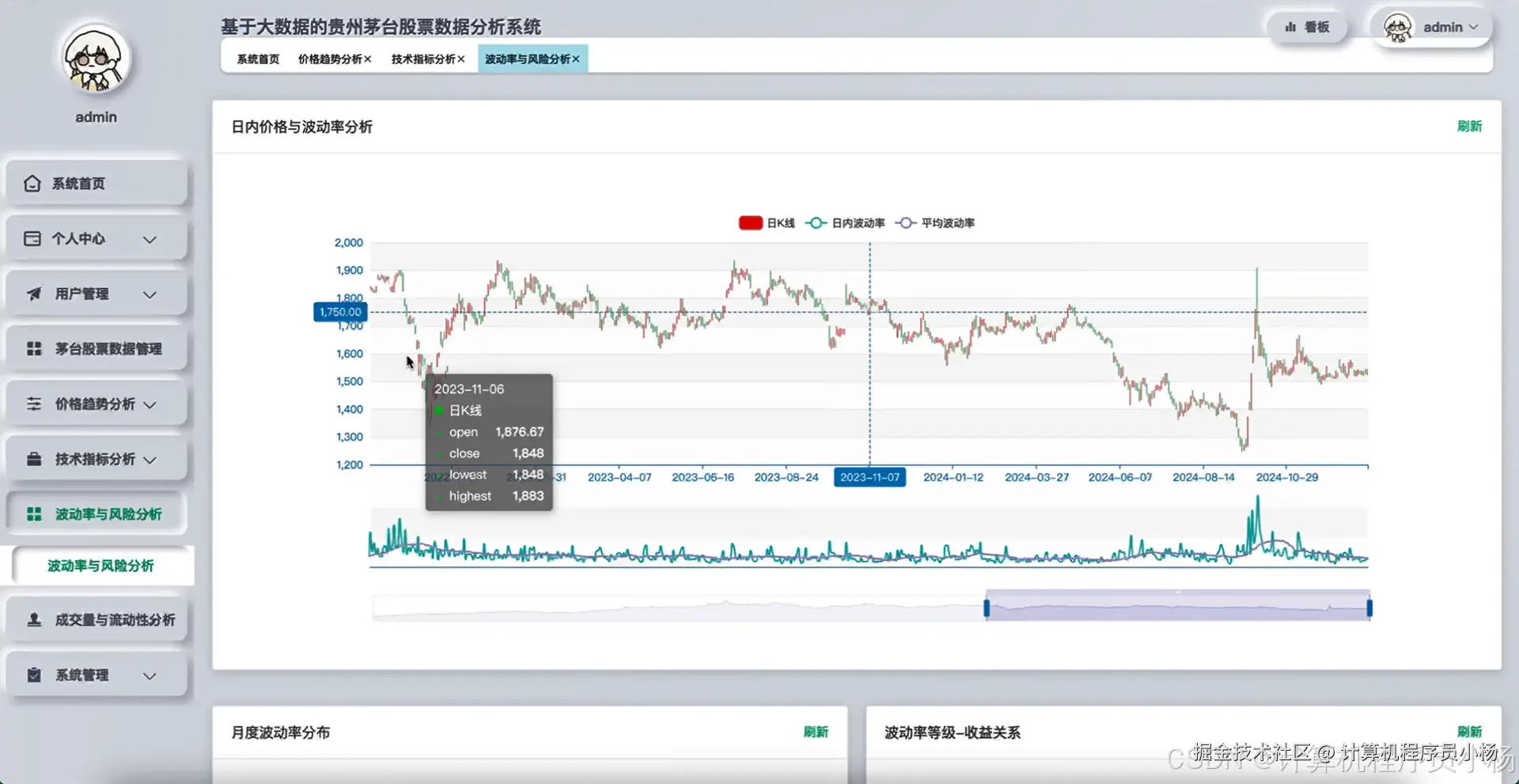

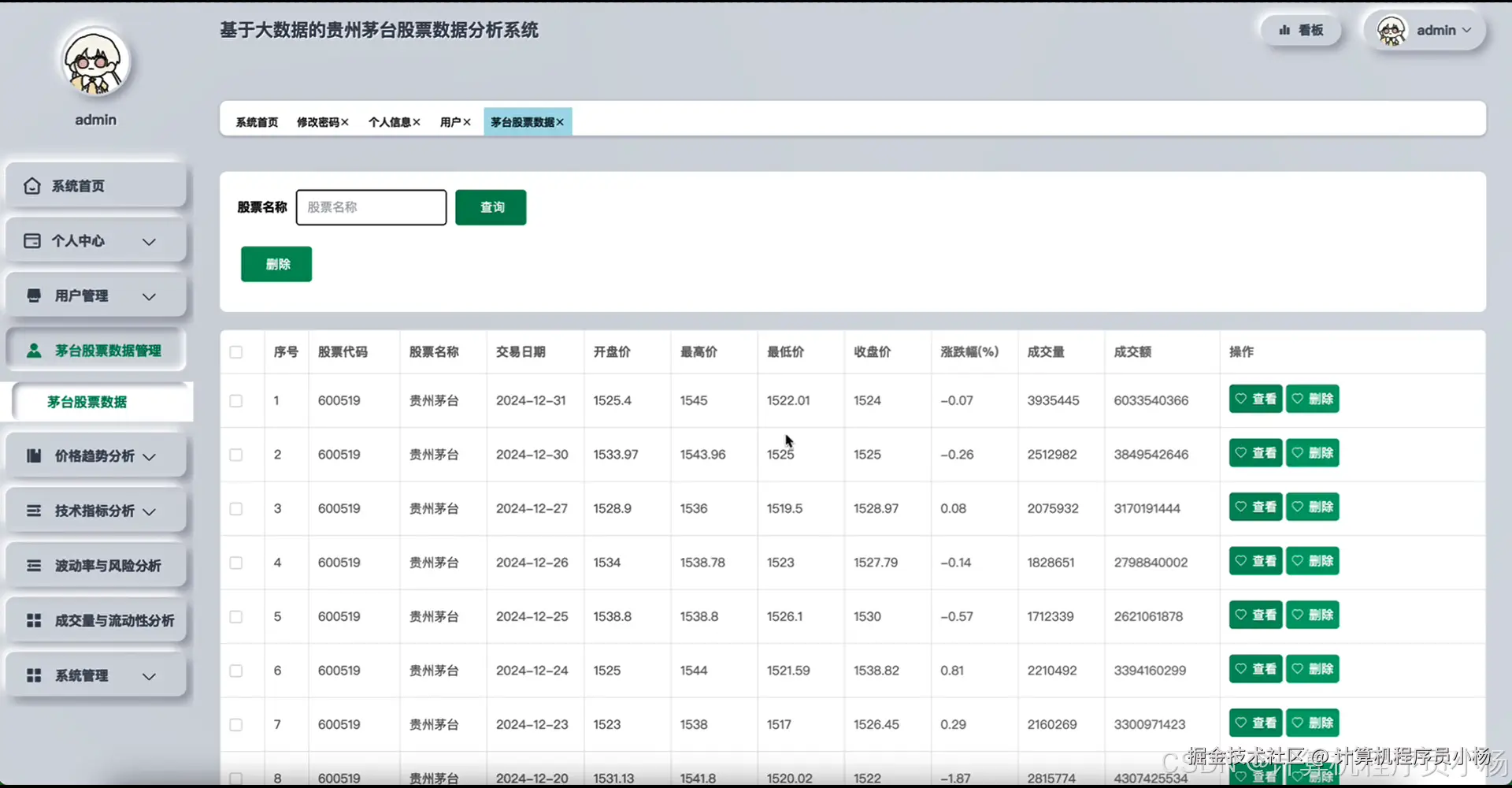

二.系统内容简介

基于大数据的贵州茅台股票数据分析系统是一个集数据采集、存储、处理和可视化分析于一体的综合性股票分析平台。系统采用Hadoop分布式文件系统作为底层数据存储架构,通过Spark大数据处理框架实现对茅台股票海量历史数据的高效分析处理。在技术实现层面,系统提供Python和Java双语言版本支持,后端分别采用Django和Spring Boot框架构建RESTful API接口,前端运用Vue.js结合ElementUI组件库打造现代化用户界面,通过ECharts图表库实现数据的直观可视化展示。系统核心功能涵盖茅台股票基础数据管理、价格趋势深度分析、技术指标计算、波动率与风险评估、成交量与流动性分析等多个维度,通过Spark SQL进行复杂查询处理,结合Pandas和NumPy进行数据科学计算,为用户提供全方位的股票分析服务。整个系统架构设计合理,技术栈搭配完善,既能满足大数据处理需求,又具备良好的用户体验和系统扩展性。

三.系统功能演示

计算机专业的你懂的:大数据毕设就选贵州茅台股票分析系统准没错|计算机毕业设计|数据可视化|数据分析

四.系统界面展示

五.系统源码展示

css

from pyspark.sql import SparkSession

from pyspark.sql.functions import *

from pyspark.sql.types import *

import pandas as pd

import numpy as np

spark = SparkSession.builder.appName("MaotaiStockAnalysis").config("spark.sql.adaptive.enabled", "true").getOrCreate()

def price_trend_analysis(stock_data):

df = spark.createDataFrame(stock_data)

df.createOrReplaceTempView("stock_temp")

trend_result = spark.sql("""

SELECT

trade_date,

close_price,

open_price,

high_price,

low_price,

LAG(close_price, 1) OVER (ORDER BY trade_date) as prev_close,

(close_price - LAG(close_price, 1) OVER (ORDER BY trade_date)) / LAG(close_price, 1) OVER (ORDER BY trade_date) * 100 as daily_return,

AVG(close_price) OVER (ORDER BY trade_date ROWS BETWEEN 4 PRECEDING AND CURRENT ROW) as ma5,

AVG(close_price) OVER (ORDER BY trade_date ROWS BETWEEN 9 PRECEDING AND CURRENT ROW) as ma10,

AVG(close_price) OVER (ORDER BY trade_date ROWS BETWEEN 19 PRECEDING AND CURRENT ROW) as ma20,

CASE

WHEN close_price > LAG(close_price, 1) OVER (ORDER BY trade_date) THEN 'UP'

WHEN close_price < LAG(close_price, 1) OVER (ORDER BY trade_date) THEN 'DOWN'

ELSE 'FLAT'

END as trend_direction

FROM stock_temp

ORDER BY trade_date

""")

trend_pandas = trend_result.toPandas()

trend_pandas['price_momentum'] = trend_pandas['daily_return'].rolling(window=5).mean()

trend_pandas['volatility_index'] = trend_pandas['daily_return'].rolling(window=10).std() * 100

trend_analysis = {

'trend_data': trend_pandas.to_dict('records'),

'avg_daily_return': float(trend_pandas['daily_return'].mean()),

'max_single_gain': float(trend_pandas['daily_return'].max()),

'max_single_loss': float(trend_pandas['daily_return'].min()),

'trend_consistency': len(trend_pandas[trend_pandas['trend_direction'] == trend_pandas['trend_direction'].mode()[0]]) / len(trend_pandas)

}

return trend_analysis

def technical_indicator_analysis(stock_data):

df = spark.createDataFrame(stock_data)

df.createOrReplaceTempView("technical_temp")

rsi_result = spark.sql("""

SELECT

trade_date,

close_price,

close_price - LAG(close_price, 1) OVER (ORDER BY trade_date) as price_change,

CASE

WHEN close_price - LAG(close_price, 1) OVER (ORDER BY trade_date) > 0

THEN close_price - LAG(close_price, 1) OVER (ORDER BY trade_date)

ELSE 0

END as gain,

CASE

WHEN close_price - LAG(close_price, 1) OVER (ORDER BY trade_date) < 0

THEN ABS(close_price - LAG(close_price, 1) OVER (ORDER BY trade_date))

ELSE 0

END as loss,

high_price,

low_price,

volume

FROM technical_temp

ORDER BY trade_date

""")

technical_pandas = rsi_result.toPandas()

technical_pandas['avg_gain'] = technical_pandas['gain'].rolling(window=14).mean()

technical_pandas['avg_loss'] = technical_pandas['loss'].rolling(window=14).mean()

technical_pandas['rs'] = technical_pandas['avg_gain'] / (technical_pandas['avg_loss'] + 0.000001)

technical_pandas['rsi'] = 100 - (100 / (1 + technical_pandas['rs']))

technical_pandas['highest_high'] = technical_pandas['high_price'].rolling(window=14).max()

technical_pandas['lowest_low'] = technical_pandas['low_price'].rolling(window=14).min()

technical_pandas['k_percent'] = ((technical_pandas['close_price'] - technical_pandas['lowest_low']) / (technical_pandas['highest_high'] - technical_pandas['lowest_low'])) * 100

technical_pandas['d_percent'] = technical_pandas['k_percent'].rolling(window=3).mean()

ema_12 = technical_pandas['close_price'].ewm(span=12).mean()

ema_26 = technical_pandas['close_price'].ewm(span=26).mean()

technical_pandas['macd_line'] = ema_12 - ema_26

technical_pandas['signal_line'] = technical_pandas['macd_line'].ewm(span=9).mean()

technical_pandas['macd_histogram'] = technical_pandas['macd_line'] - technical_pandas['signal_line']

technical_indicators = {

'indicator_data': technical_pandas[['trade_date', 'rsi', 'k_percent', 'd_percent', 'macd_line', 'signal_line', 'macd_histogram']].to_dict('records'),

'current_rsi': float(technical_pandas['rsi'].iloc[-1]) if len(technical_pandas) > 0 else 0,

'rsi_overbought_signals': len(technical_pandas[technical_pandas['rsi'] > 70]),

'rsi_oversold_signals': len(technical_pandas[technical_pandas['rsi'] < 30]),

'macd_bullish_crossovers': len(technical_pandas[(technical_pandas['macd_line'] > technical_pandas['signal_line']) & (technical_pandas['macd_line'].shift(1) <= technical_pandas['signal_line'].shift(1))]),

'macd_bearish_crossovers': len(technical_pandas[(technical_pandas['macd_line'] < technical_pandas['signal_line']) & (technical_pandas['macd_line'].shift(1) >= technical_pandas['signal_line'].shift(1))])

}

return technical_indicators

def volatility_risk_analysis(stock_data):

df = spark.createDataFrame(stock_data)

df.createOrReplaceTempView("volatility_temp")

volatility_result = spark.sql("""

SELECT

trade_date,

close_price,

high_price,

low_price,

(close_price - LAG(close_price, 1) OVER (ORDER BY trade_date)) / LAG(close_price, 1) OVER (ORDER BY trade_date) as daily_return,

((high_price - low_price) / close_price) * 100 as daily_range_pct,

volume,

volume * close_price as turnover_value

FROM volatility_temp

ORDER BY trade_date

""")

volatility_pandas = volatility_result.toPandas()

volatility_pandas['return_squared'] = volatility_pandas['daily_return'] ** 2

volatility_pandas['historical_volatility'] = volatility_pandas['daily_return'].rolling(window=20).std() * np.sqrt(252) * 100

volatility_pandas['rolling_var'] = volatility_pandas['daily_return'].rolling(window=30).var()

volatility_pandas['price_deviation'] = abs(volatility_pandas['close_price'] - volatility_pandas['close_price'].rolling(window=20).mean()) / volatility_pandas['close_price'].rolling(window=20).mean() * 100

cumulative_returns = (1 + volatility_pandas['daily_return'] / 100).cumprod() - 1

rolling_max = cumulative_returns.expanding().max()

volatility_pandas['drawdown'] = (cumulative_returns - rolling_max) * 100

volatility_pandas['max_drawdown'] = volatility_pandas['drawdown'].expanding().min()

var_95 = np.percentile(volatility_pandas['daily_return'].dropna(), 5)

var_99 = np.percentile(volatility_pandas['daily_return'].dropna(), 1)

avg_return = volatility_pandas['daily_return'].mean()

return_std = volatility_pandas['daily_return'].std()

sharpe_ratio = (avg_return / return_std) * np.sqrt(252) if return_std != 0 else 0

downside_returns = volatility_pandas['daily_return'][volatility_pandas['daily_return'] < 0]

downside_std = downside_returns.std() if len(downside_returns) > 0 else 0

sortino_ratio = (avg_return / downside_std) * np.sqrt(252) if downside_std != 0 else 0

risk_metrics = {

'volatility_data': volatility_pandas[['trade_date', 'daily_return', 'historical_volatility', 'drawdown', 'max_drawdown', 'daily_range_pct']].to_dict('records'),

'current_volatility': float(volatility_pandas['historical_volatility'].iloc[-1]) if len(volatility_pandas) > 0 else 0,

'var_95': float(var_95),

'var_99': float(var_99),

'max_historical_drawdown': float(volatility_pandas['max_drawdown'].min()),

'sharpe_ratio': float(sharpe_ratio),

'sortino_ratio': float(sortino_ratio),

'volatility_trend': 'INCREASING' if volatility_pandas['historical_volatility'].iloc[-5:].mean() > volatility_pandas['historical_volatility'].iloc[-10:-5].mean() else 'DECREASING'

}

return risk_metrics六.系统文档展示