大家好,我是花姐。经常有小伙伴问我:"股票的支撑位、压力位怎么找?有没有办法用 Python 程序自动算出来?"

之前我们讲了通过枢轴点、局部极值 2种方法来确定压力和支撑位置,今天我们来说说均线簇法确定压力和支撑位置。

开始前的准备

我这里用的行情数据源是 xtquant + miniQMT 。 后续示例里会用到一些常见的 Python 库:pandas, numpy, matplotlib,进阶部分还会涉及 scipy, sklearn。在实际运行代码之前,记得先把环境配置好:

bash

pip install pandas numpy matplotlib scipy scikit-learn xtquant这样就能避免因为依赖缺失导致的报错啦。

以下是一个基于xtquant + miniQMT获取股票行情的方法,后面的行情Dataframe数据都会通过这个方法来获取:

python

def get_hq(code,start_date='19900101',period='1d',dividend_type='front_ratio',count=-1):

'''

基于xtquant下载某个股票的历史行情

盘中运行最后一个K里存了最新的行情

period 1d 1w 1mon

dividend_type - 除权方式,用于K线数据复权计算,对tick等其他周期数据无效

none 不复权

front 前复权

back 后复权

front_ratio 等比前复权

back_ratio 等比后复权

'''

xtdata.enable_hello = False

xtdata.download_history_data(stock_code=code, period='1d',incrementally=True)

history_data = xtdata.get_market_data_ex(['open','high','low','close','volume','amount','preClose','suspendFlag'],[code],period=period,start_time=start_date,count=count,dividend_type=dividend_type)

print(history_data)

df = history_data[code]

df.index = pd.to_datetime(df.index.astype(str), format='%Y%m%d')

df['date'] = df.index

return df1. 由来与直观理解

在股市里,价格上涨或者下跌往往会遇到一些"阻力"或"支撑",这个概念大家可能听得多,但怎么量化呢?

于是就有了均线簇的概念:

- 我们把多条均线同时画在一张K线图上

- 当这些均线在某个价格区间聚集时,就形成了"均线簇"

- 均线簇的密集区往往对应压力位(价格上不去)或支撑位(价格不跌破)

直观理解:

- 想象几条橡皮筋同时捆在股票价格上方或下方,价格想突破或跌破时就像要拉开橡皮筋,会有阻力

- 这就是均线簇在做的事情:用过去价格的平均值,画出价格心理关口

2. 数学定义与原理

- 简单移动平均线(SMA)

SMAn(t)=n1i=0∑n−1Pt−i

- n 是窗口大小(天数)

- Pt 是第 t 天的收盘价

- 均线簇的形成条件

- 当多条不同周期均线之间的价格差异非常小,比如5日、10日、20日、30日均线同时靠近同一个价格区间

- 数学上可以用均线标准差 或者均线最大最小差值来量化:

MA_spread=max(MA1,MA2,...,MAn)−min(MA1,MA2,...,MAn)

- 当

MA_spread很小,说明均线聚集形成簇

原理:

- 均线簇反映了市场短中期均衡状态

- 多空力量在这个价格附近相对均衡

- 突破均线簇往往伴随成交量放大,是典型的趋势启动信号

3. 常用算法

- 简单聚合均线

- 选择5条或以上不同周期均线

- 计算均线最大最小差值

- 小于阈值时判定为均线簇

- 均线簇密度算法(进阶)

- 用均线标准差衡量密集度:

MA_std=std(MA1,MA2,...,MAn)

- 标准差越小,均线聚集越密集

- 可以设置动态阈值,如过去20日均值的20%

- 支撑/压力判定

- 均线簇在股价上方 → 压力位

- 均线簇在股价下方 → 支撑位

4. 实战Python代码

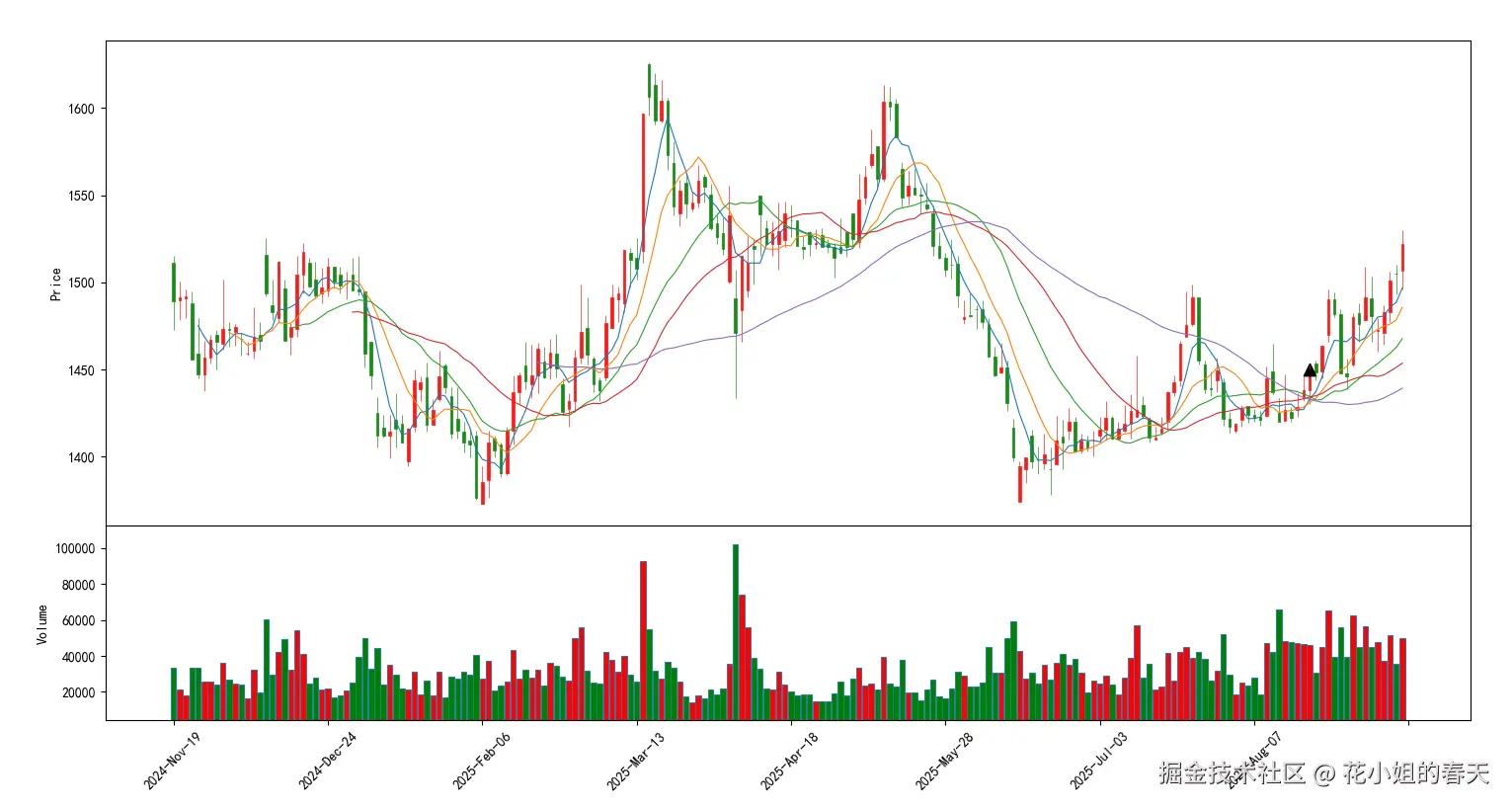

均线簇 ≈ 市场在蓄力,方向不确定,但一旦突破,往往容易走出一波行情 🚀

4.1 使用简单聚合均线

计算思路

-

1 算均线 → 5日、10日、20日、30日、60日

-

2.判断是否簇 → 如果这些均线的最高值和最低值之间的差距小于价格的1%,就算是"簇"。

-

3.找第一个点 → 我们只想标记簇刚出现的时候(而不是整个簇区域)。

示例代码

python

from xtquant import xtdata

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import mplfinance as mpf

def detect_ma_clusters(df, ma_periods=[5, 10, 20, 30, 60], price_col='close', threshold_pct=0.01):

"""

根据均线计算均线簇,并只返回连续簇的第一个点

"""

df = df.copy()

print(df)

# 1. 计算均线

for period in ma_periods:

df[f'MA_{period}'] = df[price_col].rolling(window=period).mean()

df = df.dropna(subset=[f'MA_{p}' for p in ma_periods])

print(df)

ma_cols = [f'MA_{p}' for p in ma_periods]

# 2. 计算均线最大最小值及差值

df['MA_max'] = df[ma_cols].max(axis=1)

df['MA_min'] = df[ma_cols].min(axis=1)

df['MA_spread'] = df['MA_max'] - df['MA_min']

# 3. 判断均线簇(相对价格)

df['Cluster'] = df['MA_spread'] / df[price_col] < threshold_pct

# 4. 只取连续簇的第一个值

# shift(1) 表示前一天的 Cluster 状态

df['Cluster_start'] = (df['Cluster'] & ~df['Cluster'].shift(1).fillna(False))

# 取出第一个点

cluster = df.loc[df['Cluster_start'], price_col]

return cluster

def draw_ma_clusters(df, cluster, ma_periods=[5, 10, 20, 30, 60]):

# mplfinance 要求 DataFrame 索引为日期,并包含 Open, High, Low, Close

mpf_data = df[['open','high','low','close','volume']].copy()

mpf_data.index = pd.DatetimeIndex(mpf_data.index)

apds = []

# 准备支撑位/压力位标记

cluster_y = np.full(len(mpf_data), np.nan)

# 填充支撑位/压力位对应价格

if len(cluster) > 0:

for date, price in cluster.items():

if date in mpf_data.index:

idx = mpf_data.index.get_loc(date)

cluster_y[idx] = price

apds.append(mpf.make_addplot(cluster_y, type='scatter', markersize=80, marker='^', color='black'))

mc = mpf.make_marketcolors(up='r', down='g', inherit=True)

s = mpf.make_mpf_style(marketcolors=mc,rc={'font.family': 'SimHei'})

mpf.plot(

mpf_data,

type='candle',

style=s,

title="K线及均线簇",

mav=ma_periods,

addplot=apds,

volume=True,

figsize=(14,7)

)

if __name__ == "__main__":

code = '600519.SH' # 贵州茅台

df = get_hq(code, start_date='20200101', period='1d', count=200)

cluster = detect_ma_clusters(df, ma_periods=[5, 10, 20, 30, 60])

draw_ma_clusters(df, cluster, ma_periods=[5, 10, 20, 30, 60])

4.2 使用均线簇密度算法(进阶)

计算思路

-

计算不同周期的均线;

-

计算这些均线的标准差

MA_std; -

用动态阈值:

MA_std < rolling_mean(MA_std, 20) * factor来判定是否属于"均线簇"; -

依然只取连续簇的第一个点。

示例代码

python

from xtquant import xtdata

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import mplfinance as mpf

def draw_ma_clusters(df, cluster, ma_periods=[5, 10, 20, 30, 60]):

# mplfinance 要求 DataFrame 索引为日期,并包含 Open, High, Low, Close

mpf_data = df[['open','high','low','close','volume']].copy()

mpf_data.index = pd.DatetimeIndex(mpf_data.index)

apds = []

# 准备支撑位/压力位标记

cluster_y = np.full(len(mpf_data), np.nan)

# 填充支撑位/压力位对应价格

# 支撑位绘制

if len(cluster) > 0:

for date, price in cluster.items():

if date in mpf_data.index:

idx = mpf_data.index.get_loc(date)

cluster_y[idx] = price

apds.append(mpf.make_addplot(cluster_y, type='scatter', markersize=80, marker='^', color='black'))

mc = mpf.make_marketcolors(up='r', down='g', inherit=True)

s = mpf.make_mpf_style(marketcolors=mc,rc={'font.family': 'SimHei'})

mpf.plot(

mpf_data,

type='candle',

style=s,

title="K线及均线簇",

mav=ma_periods,

addplot=apds,

volume=True,

figsize=(14,7)

)

def detect_ma_clusters_std(df, ma_periods=[5, 10, 20, 30, 60], price_col='close',

lookback=20, factor=0.2):

"""

基于均线标准差来检测均线簇,并只返回连续簇的第一个点

参数:

df : DataFrame,行情数据

ma_periods : list,均线周期

price_col : str,收盘价字段

lookback : int,动态阈值的回看窗口

factor : float,动态阈值因子(比如0.2表示20%)

"""

df = df.copy()

# 1. 计算均线

for period in ma_periods:

df[f'MA_{period}'] = df[price_col].rolling(window=period).mean()

df = df.dropna(subset=[f'MA_{p}' for p in ma_periods])

ma_cols = [f'MA_{p}' for p in ma_periods]

# 2. 计算均线标准差

df['MA_std'] = df[ma_cols].std(axis=1)

# 3. 计算动态阈值:过去 lookback 日 MA_std 均值 * factor

df['Threshold'] = df['MA_std'].rolling(window=lookback).mean() * factor

# 4. 判断均线簇

df['Cluster'] = df['MA_std'] < df['Threshold']

# 5. 只取连续簇的第一个点

df['Cluster_start'] = (df['Cluster'] & ~df['Cluster'].shift(1).fillna(False))

# 取出第一个点(收盘价作为簇的价格)

cluster = df.loc[df['Cluster_start'], price_col]

return cluster

if __name__ == "__main__":

code = '600519.SH' # 贵州茅台

df = get_hq(code, start_date='20200101', period='1d', count=200)

cluster = detect_ma_clusters_std(df, ma_periods=[5, 10, 20, 30, 60])

draw_ma_clusters(df, cluster, ma_periods=[5, 10, 20, 30, 60])

今天关于寻找股票支撑与压力位的均线簇法就写到这里了,更高级的用法有兴趣的朋友可以结合AI来自由探索,花姐这里只做简单科普抛砖引玉。

下一篇我们介绍通过斐波那契回撤寻找股票支撑与压力位。