import numpy as np

import matplotlib.pyplot as plt

from scipy import stats

from typing import List, Callable

import seaborn as sns

from scipy.special import comb

def true_pass_at_k(p: float, k: int) -> float:

"""True pass@k value: 1 - (1-p)^k"""

return 1 - (1 - p) ** k

def bootstrap_estimator(samples: List[bool], k: int, n_bootstrap: int = 1000) -> float:

"""Bootstrap estimator for pass@k"""

n = len(samples)

if n == 0:

return 0.0

bootstrap_estimates = []

for _ in range(n_bootstrap):

# Sample with replacement

bootstrap_sample = np.random.choice(samples, size=min(k, n), replace=True)

bootstrap_estimates.append(np.any(bootstrap_sample))

return np.mean(bootstrap_estimates)

# Set style for better plots

plt.style.use('seaborn-v0_8')

sns.set_palette("husl")

true_p = 0.3

max_samples=100

n_trials=200

k_values = [1, 3, 5, 10, 20]

# Colors for different k values

# Set up the plot

fig, axes = plt.subplots(1, 1, figsize=(15, 12))

colors = plt.cm.viridis(np.linspace(0, 1, len(k_values)))

ax = axes

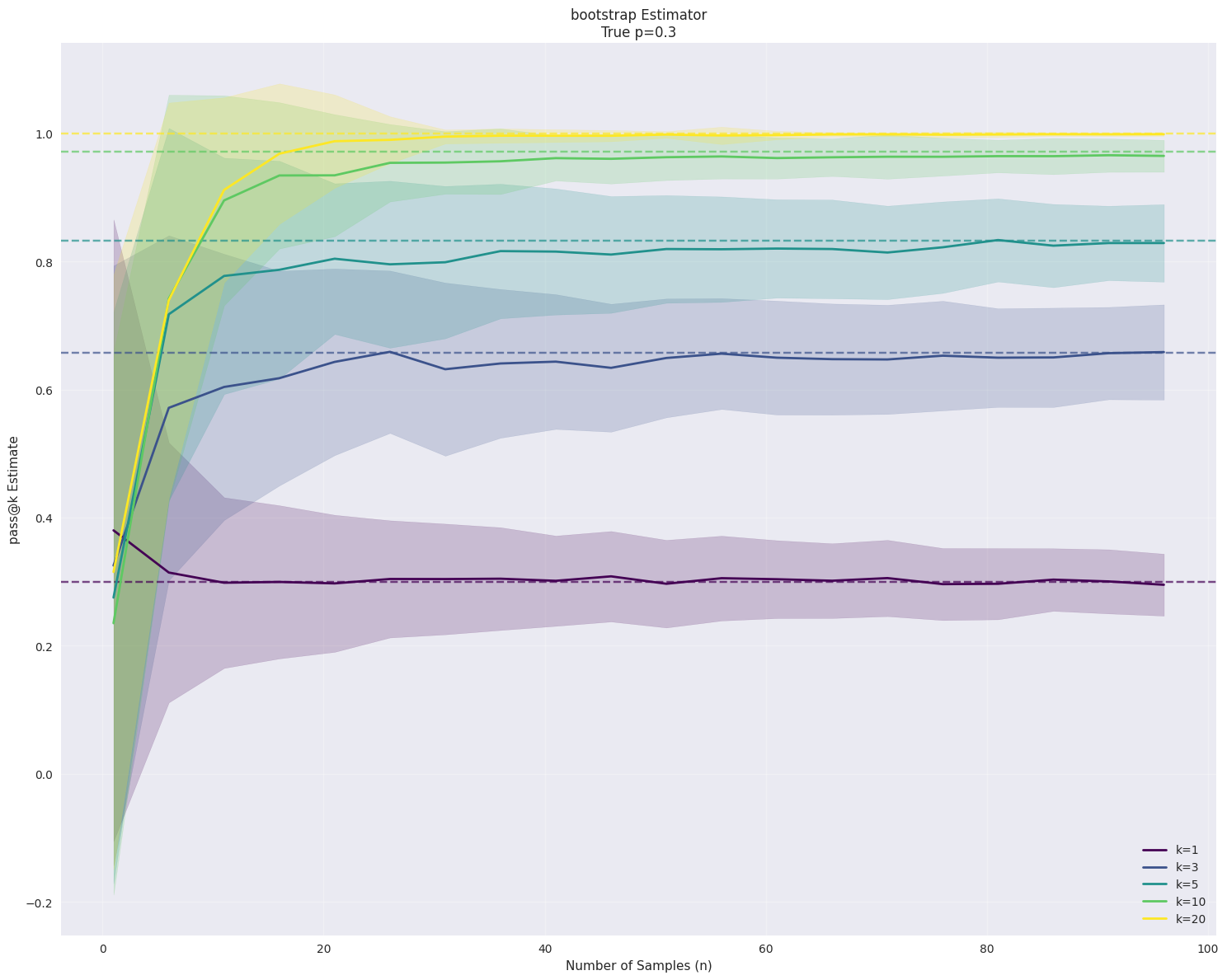

for k_idx, k in enumerate(k_values):

# True value

true_value = true_pass_at_k(true_p, k)

# Store estimates for different sample sizes

sample_sizes = []

estimates_mean = []

estimates_std = []

biases = []

for n_samples in range(1, max_samples + 1, 5):

trial_estimates = []

for trial in range(n_trials):

# Generate samples

samples = np.random.binomial(1, true_p, n_samples).astype(bool)

estimate = bootstrap_estimator(samples.tolist(), k, 500)

trial_estimates.append(estimate)

sample_sizes.append(n_samples)

estimates_mean.append(np.mean(trial_estimates))

estimates_std.append(np.std(trial_estimates))

biases.append(np.mean(trial_estimates) - true_value)

# Plot mean estimates

ax.plot(sample_sizes, estimates_mean,

color=colors[k_idx], label=f'k={k}', linewidth=2)

# Add shaded region for ±1 std

ax.fill_between(sample_sizes,

np.array(estimates_mean) - np.array(estimates_std),

np.array(estimates_mean) + np.array(estimates_std),

alpha=0.2, color=colors[k_idx])

# Plot true value as horizontal line

ax.axhline(y=true_value, color=colors[k_idx], linestyle='--', alpha=0.7)

ax.set_xlabel('Number of Samples (n)')

ax.set_ylabel('pass@k Estimate')

ax.set_title(f'bootstrap Estimator\n'

f'True p={true_p}')

ax.legend()

ax.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

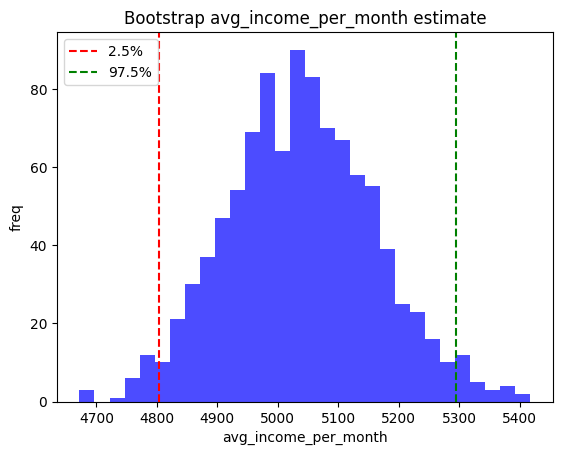

输出如下所示,在样本数n比较小的时候,方差还是比较大的。

3 综合模拟对比

这里进一步对比bootstrap估计和其他估计模拟估计手段。

3.1 bootstrap

bootstrap模拟过程代码示例如下。

复制代码

def bootstrap_estimator(samples: List[bool], k: int, n_bootstrap: int = 1000) -> float:

"""Bootstrap estimator for pass@k"""

n = len(samples)

if n == 0:

return 0.0

bootstrap_estimates = []

for _ in range(n_bootstrap):

# Sample with replacement

bootstrap_sample = np.random.choice(samples, size=min(k, n), replace=True)

bootstrap_estimates.append(np.any(bootstrap_sample))

return np.mean(bootstrap_estimates)

3.2 monte carlo

monte carlo模拟估计代码示例如下

复制代码

def monte_carlo_estimator(samples: List[bool], k: int, n_simulations: int = 1000) -> float:

"""Monte Carlo estimator for pass@k"""

n = len(samples)

if n == 0:

return 0.0

successes = 0

for _ in range(n_simulations):

# Randomly select k samples without replacement

selected_indices = np.random.choice(n, size=min(k, n), replace=False)

selected_samples = [samples[i] for i in selected_indices]

if np.any(selected_samples):

successes += 1

return successes / n_simulations

3.3 直接模拟

直接模拟代码示例如下

复制代码

def direct_estimator(samples: List[bool], k: int) -> float:

"""Direct estimator using sample proportion"""

n = len(samples)

if n == 0:

return 0.0

# Take first k samples (or all if n < k)

selected_samples = samples[:min(k, n)]

return float(np.any(selected_samples))

3.4 unbiased模拟

无偏模拟,也就是OpenAI在HumanEval采用的模拟方法,代码示例如下

复制代码

def unbiased_estimator(samples: List[bool], k: int) -> float:

"""Unbiased estimator using combinatorial approach"""

n = len(samples)

if n < k:

return float(np.any(samples)) # Fallback if not enough samples

# Count number of successes

c = np.sum(samples)

if c == 0:

return 0.0

# Unbiased estimator: 1 - (n-c choose k) / (n choose k)

n_choose_k = comb(n, k)

if n - c < k:

return 1.0

n_minus_c_choose_k = comb(n - c, k)

return 1 - n_minus_c_choose_k / n_choose_k

3.4 综合对比

综合以上多种模拟方案,进行对比示例。

复制代码

import numpy as np

import matplotlib.pyplot as plt

from scipy import stats

from typing import List, Callable

import seaborn as sns

from scipy.special import comb

# Set style for better plots

plt.style.use('seaborn-v0_8')

sns.set_palette("husl")

def true_pass_at_k(p: float, k: int) -> float:

"""True pass@k value: 1 - (1-p)^k"""

return 1 - (1 - p) ** k

def bootstrap_estimator(samples: List[bool], k: int, n_bootstrap: int = 1000) -> float:

"""Bootstrap estimator for pass@k"""

n = len(samples)

if n == 0:

return 0.0

bootstrap_estimates = []

for _ in range(n_bootstrap):

# Sample with replacement

bootstrap_sample = np.random.choice(samples, size=min(k, n), replace=True)

bootstrap_estimates.append(np.any(bootstrap_sample))

return np.mean(bootstrap_estimates)

def direct_estimator(samples: List[bool], k: int) -> float:

"""Direct estimator using sample proportion"""

n = len(samples)

if n == 0:

return 0.0

# Take first k samples (or all if n < k)

selected_samples = samples[:min(k, n)]

return float(np.any(selected_samples))

def unbiased_estimator(samples: List[bool], k: int) -> float:

"""Unbiased estimator using combinatorial approach"""

n = len(samples)

if n < k:

return float(np.any(samples)) # Fallback if not enough samples

# Count number of successes

c = np.sum(samples)

if c == 0:

return 0.0

# Unbiased estimator: 1 - (n-c choose k) / (n choose k)

n_choose_k = comb(n, k)

if n - c < k:

return 1.0

n_minus_c_choose_k = comb(n - c, k)

return 1 - n_minus_c_choose_k / n_choose_k

def monte_carlo_estimator(samples: List[bool], k: int, n_simulations: int = 1000) -> float:

"""Monte Carlo estimator for pass@k"""

n = len(samples)

if n == 0:

return 0.0

successes = 0

for _ in range(n_simulations):

# Randomly select k samples without replacement

selected_indices = np.random.choice(n, size=min(k, n), replace=False)

selected_samples = [samples[i] for i in selected_indices]

if np.any(selected_samples):

successes += 1

return successes / n_simulations

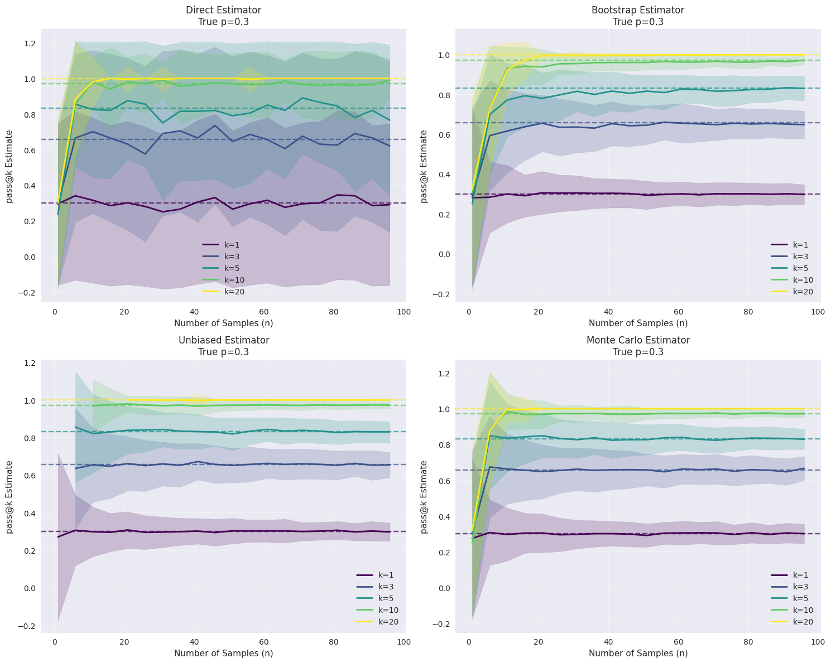

def analyze_estimators(true_p: float = 0.3, max_samples: int = 100, k_values: List[int] = None, n_trials: int = 100):

"""Analyze bias and variance of different pass@k estimators"""

if k_values is None:

k_values = [1, 3, 5, 10, 20]

estimators = {

'Direct': direct_estimator,

'Bootstrap': lambda samples, k: bootstrap_estimator(samples, k, 500),

'Unbiased': unbiased_estimator,

'Monte Carlo': lambda samples, k: monte_carlo_estimator(samples, k, 500)

}

# Set up the plot

fig, axes = plt.subplots(2, 2, figsize=(15, 12))

axes = axes.flatten()

# Colors for different k values

colors = plt.cm.viridis(np.linspace(0, 1, len(k_values)))

for idx, (estimator_name, estimator_func) in enumerate(estimators.items()):

ax = axes[idx]

for k_idx, k in enumerate(k_values):

# True value

true_value = true_pass_at_k(true_p, k)

# Store estimates for different sample sizes

sample_sizes = []

estimates_mean = []

estimates_std = []

biases = []

for n_samples in range(1, max_samples + 1, 5):

if n_samples < k and estimator_name == 'Unbiased':

continue # Unbiased estimator requires n >= k

trial_estimates = []

for trial in range(n_trials):

# Generate samples

samples = np.random.binomial(1, true_p, n_samples).astype(bool)

estimate = estimator_func(samples.tolist(), k)

trial_estimates.append(estimate)

sample_sizes.append(n_samples)

estimates_mean.append(np.mean(trial_estimates))

estimates_std.append(np.std(trial_estimates))

biases.append(np.mean(trial_estimates) - true_value)

# Plot mean estimates

ax.plot(sample_sizes, estimates_mean,

color=colors[k_idx], label=f'k={k}', linewidth=2)

# Add shaded region for ±1 std

ax.fill_between(sample_sizes,

np.array(estimates_mean) - np.array(estimates_std),

np.array(estimates_mean) + np.array(estimates_std),

alpha=0.2, color=colors[k_idx])

# Plot true value as horizontal line

ax.axhline(y=true_value, color=colors[k_idx], linestyle='--', alpha=0.7)

ax.set_xlabel('Number of Samples (n)')

ax.set_ylabel('pass@k Estimate')

ax.set_title(f'{estimator_name} Estimator\n'

f'True p={true_p}')

ax.legend()

ax.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

# Plot bias and variance comparison

plot_bias_variance_comparison(estimators, true_p, max_samples, k_values, n_trials)

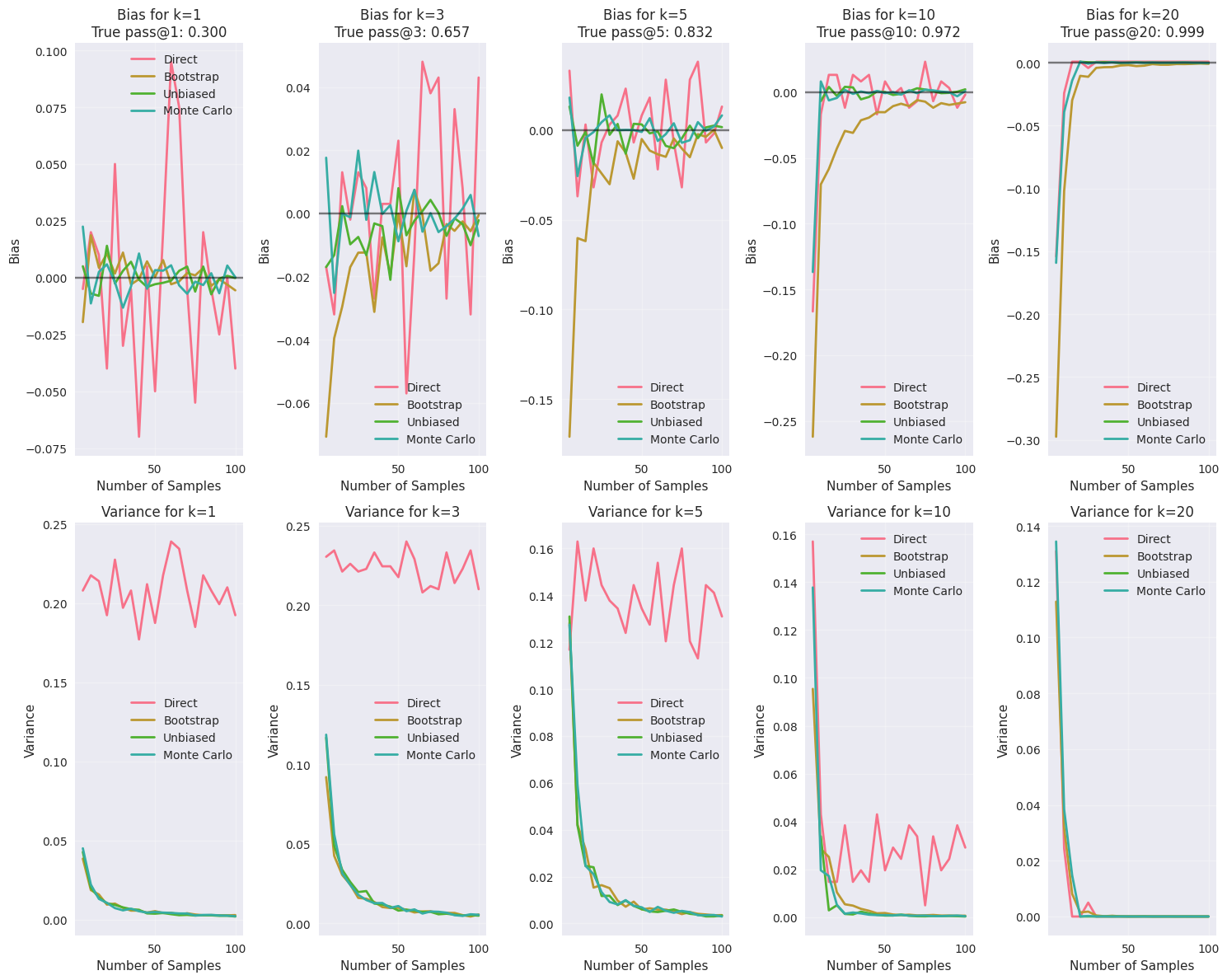

def plot_bias_variance_comparison(estimators, true_p, max_samples, k_values, n_trials):

"""Plot bias and variance comparison across estimators"""

fig, axes = plt.subplots(2, 5, figsize=(15, 12))

for plot_idx, k in enumerate(k_values[:5]): # Plot first 5 k values

print(f"plot_idx: {plot_idx}, k: {k}")

print()

ax_bias = axes[0, plot_idx]

ax_variance = axes[1, plot_idx]

true_value = true_pass_at_k(true_p, k)

for estimator_name, estimator_func in estimators.items():

biases = []

variances = []

sample_sizes = []

for n_samples in range(5, max_samples + 1, 5):

if n_samples < k and estimator_name == 'Unbiased':

continue

trial_estimates = []

for trial in range(n_trials):

samples = np.random.binomial(1, true_p, n_samples).astype(bool)

estimate = estimator_func(samples.tolist(), k)

trial_estimates.append(estimate)

sample_sizes.append(n_samples)

bias = np.mean(trial_estimates) - true_value

variance = np.var(trial_estimates)

biases.append(bias)

variances.append(variance)

ax_bias.plot(sample_sizes, biases, label=estimator_name, linewidth=2)

ax_variance.plot(sample_sizes, variances, label=estimator_name, linewidth=2)

ax_bias.set_title(f'Bias for k={k}\nTrue pass@{k}: {true_value:.3f}')

ax_bias.set_xlabel('Number of Samples')

ax_bias.set_ylabel('Bias')

ax_bias.legend()

ax_bias.grid(True, alpha=0.3)

ax_bias.axhline(y=0, color='black', linestyle='-', alpha=0.5)

ax_variance.set_title(f'Variance for k={k}')

ax_variance.set_xlabel('Number of Samples')

ax_variance.set_ylabel('Variance')

ax_variance.legend()

ax_variance.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

def plot_pass_at_k_curves(p_values: List[float] = None, k_max: int = 50):

"""Plot theoretical pass@k curves for different p values"""

if p_values is None:

p_values = [0.1, 0.3, 0.5, 0.7, 0.9]

plt.figure(figsize=(12, 8))

k_range = np.arange(1, k_max + 1)

for p in p_values:

pass_values = [true_pass_at_k(p, k) for k in k_range]

plt.plot(k_range, pass_values, label=f'p={p}', linewidth=3)

plt.xlabel('k (number of samples)')

plt.ylabel('pass@k')

plt.title('Theoretical pass@k Curves for Different Success Probabilities')

plt.legend()

plt.grid(True, alpha=0.3)

plt.ylim(0, 1)

plt.show()

# Run the analysis

if __name__ == "__main__":

print("Plotting theoretical pass@k curves...")

# plot_pass_at_k_curves()

print("\nAnalyzing estimator performance...")

analyze_estimators(true_p=0.3, max_samples=100, n_trials=200)

# print("\nAnalyzing estimator performance with different p...")

# analyze_estimators(true_p=0.1, max_samples=100, n_trials=200)