目录

[一、Load Data 加载数据](#一、Load Data 加载数据)

[二、Define cross-validation parameters 定义交叉验证参数](#二、Define cross-validation parameters 定义交叉验证参数)

[三、Run cross-validation 运行交叉验证](#三、Run cross-validation 运行交叉验证)

[四、Evaluate Results 评估结果](#四、Evaluate Results 评估结果)

这篇文章其实和前面的差不多,作者可能是为了加深印象,又举了一个例子。

This paragraph is similar to those before.

一、Load Data 加载数据

python

import warnings

warnings.filterwarnings('ignore')

from pathlib import Path

import sys, os

from time import time

import pandas as pd

import numpy as np

from scipy.stats import spearmanr

from sklearn.metrics import roc_auc_score

from sklearn.linear_model import LogisticRegression

from sklearn.pipeline import Pipeline

from sklearn.preprocessing import StandardScaler

import seaborn as sns

import matplotlib.pyplot as plt

# sys.path.insert(1, os.path.join(sys.path[0], '..'))

# from utils import MultipleTimeSeriesCV

sns.set_style('darkgrid')

idx = pd.IndexSlice

YEAR = 252

# Load Data

with pd.HDFStore('data.h5') as store:

data = (store['model_data']

.dropna()

.drop(['open', 'close', 'low', 'high'], axis=1))

data = data.drop([c for c in data.columns if 'year' in c or 'lag' in c], axis=1)

# Select Investment Universe

data = data[data.dollar_vol_rank<100]

# Create Model Data

y = data.filter(like='target')

X = data.drop(y.columns, axis=1)

X = X.drop(['dollar_vol', 'dollar_vol_rank', 'volume', 'consumer_durables'], axis=1)二、Define cross-validation parameters 定义交叉验证参数

这里本人为了降低调试难度,没有用到utils.py文件

python

# https://github.com/stefan-jansen/machine-learning-for-trading/blob/main/utils.py

class MultipleTimeSeriesCV:

"""Generates tuples of train_idx, test_idx pairs

Assumes the MultiIndex contains levels 'symbol' and 'date'

purges overlapping outcomes"""

def __init__(self,

n_splits=3,

train_period_length=126,

test_period_length=21,

lookahead=None,

date_idx='date',

shuffle=False):

self.n_splits = n_splits

self.lookahead = lookahead

self.test_length = test_period_length

self.train_length = train_period_length

self.shuffle = shuffle

self.date_idx = date_idx

def split(self, X, y=None, groups=None):

unique_dates = X.index.get_level_values(self.date_idx).unique()

days = sorted(unique_dates, reverse=True)

split_idx = []

for i in range(self.n_splits):

test_end_idx = i * self.test_length

test_start_idx = test_end_idx + self.test_length

train_end_idx = test_start_idx + self.lookahead - 1

train_start_idx = train_end_idx + self.train_length + self.lookahead - 1

split_idx.append([train_start_idx, train_end_idx,

test_start_idx, test_end_idx])

dates = X.reset_index()[[self.date_idx]]

for train_start, train_end, test_start, test_end in split_idx:

train_idx = dates[(dates[self.date_idx] > days[train_start])

& (dates[self.date_idx] <= days[train_end])].index

test_idx = dates[(dates[self.date_idx] > days[test_start])

& (dates[self.date_idx] <= days[test_end])].index

if self.shuffle:

np.random.shuffle(list(train_idx))

yield train_idx.to_numpy(), test_idx.to_numpy()

def get_n_splits(self, X, y, groups=None):

return self.n_splits

train_period_length = 63

test_period_length = 10

lookahead =1

n_splits = int(3 * YEAR/test_period_length)

cv = MultipleTimeSeriesCV(n_splits=n_splits,

test_period_length=test_period_length,

lookahead=lookahead,

train_period_length=train_period_length)

target = f'target_{lookahead}d'

y.loc[:, 'label'] = (y[target] > 0).astype(int)

y.label.value_counts()

Cs = np.logspace(-5, 5, 11)

cols = ['C', 'date', 'auc', 'ic', 'pval']从这里就可以看出:

y.loc[:, 'label'] = (y[target] > 0).astype(int)

y.label.value_counts()1 56486

0 53189

Name: label, dtype: int64这是一个二分类任务。

三、Run cross-validation 运行交叉验证

python

# %%time

log_coeffs, log_scores, log_predictions = {}, [], []

for C in Cs:

print(C)

model = LogisticRegression(C=C,

fit_intercept=True,

random_state=42,

n_jobs=-1)

pipe = Pipeline([

('scaler', StandardScaler()),

('model', model)])

ics = aucs = 0

start = time()

coeffs = []

for i, (train_idx, test_idx) in enumerate(cv.split(X), 1):

X_train, y_train, = X.iloc[train_idx], y.label.iloc[train_idx]

pipe.fit(X=X_train, y=y_train)

X_test, y_test = X.iloc[test_idx], y.label.iloc[test_idx]

actuals = y[target].iloc[test_idx]

if len(y_test) < 10 or len(np.unique(y_test)) < 2:

continue

y_score = pipe.predict_proba(X_test)[:, 1]

auc = roc_auc_score(y_score=y_score, y_true=y_test)

actuals = y[target].iloc[test_idx]

ic, pval = spearmanr(y_score, actuals)

log_predictions.append(y_test.to_frame('labels').assign(

predicted=y_score, C=C, actuals=actuals))

date = y_test.index.get_level_values('date').min()

log_scores.append([C, date, auc, ic * 100, pval])

coeffs.append(pipe.named_steps['model'].coef_)

ics += ic

aucs += auc

if i % 10 == 0:

print(f'\t{time()-start:5.1f} | {i:03} | {ics/i:>7.2%} | {aucs/i:>7.2%}')

log_coeffs[C] = np.mean(coeffs, axis=0).squeeze()输出:

python

1e-05

7.3 | 010 | -0.21% | 50.30%

9.3 | 020 | 2.42% | 51.99%

10.9 | 030 | 3.10% | 52.11%

13.2 | 040 | 3.49% | 52.07%

15.1 | 050 | 4.01% | 52.47%

16.5 | 060 | 3.91% | 52.25%

17.7 | 070 | 4.63% | 52.54%

0.0001

1.4 | 010 | -0.09% | 50.42%

2.6 | 020 | 2.57% | 52.09%

4.0 | 030 | 3.32% | 52.30%

5.3 | 040 | 3.47% | 52.14%

6.7 | 050 | 3.98% | 52.52%

8.0 | 060 | 3.92% | 52.29%

9.4 | 070 | 4.70% | 52.60%

0.001

1.5 | 010 | 0.30% | 50.71%

2.8 | 020 | 2.73% | 52.15%

4.1 | 030 | 3.58% | 52.48%

5.5 | 040 | 3.21% | 52.09%

6.9 | 050 | 3.84% | 52.52%

8.2 | 060 | 3.98% | 52.33%

9.6 | 070 | 4.78% | 52.66%

0.01

1.5 | 010 | 0.51% | 50.82%

2.6 | 020 | 2.56% | 51.96%

3.9 | 030 | 3.55% | 52.35%

5.2 | 040 | 3.02% | 51.90%

6.4 | 050 | 3.88% | 52.47%

7.6 | 060 | 4.05% | 52.28%

8.8 | 070 | 4.76% | 52.58%

0.1

1.3 | 010 | 0.44% | 50.74%

2.8 | 020 | 2.28% | 51.74%

4.7 | 030 | 3.32% | 52.17%

6.1 | 040 | 2.77% | 51.71%

7.8 | 050 | 3.65% | 52.30%

9.2 | 060 | 3.82% | 52.12%

10.8 | 070 | 4.46% | 52.40%

1.0

1.9 | 010 | 0.42% | 50.72%

2.9 | 020 | 2.22% | 51.69%

4.3 | 030 | 3.26% | 52.12%

5.9 | 040 | 2.70% | 51.66%

7.3 | 050 | 3.58% | 52.26%

8.9 | 060 | 3.74% | 52.07%

10.1 | 070 | 4.37% | 52.35%

10.0

1.6 | 010 | 0.42% | 50.72%

3.1 | 020 | 2.21% | 51.68%

5.0 | 030 | 3.25% | 52.12%

6.9 | 040 | 2.69% | 51.66%

9.0 | 050 | 3.58% | 52.25%

10.3 | 060 | 3.73% | 52.06%

12.1 | 070 | 4.36% | 52.34%

100.0

1.5 | 010 | 0.42% | 50.72%

3.4 | 020 | 2.21% | 51.68%

4.9 | 030 | 3.25% | 52.12%

6.5 | 040 | 2.69% | 51.66%

8.0 | 050 | 3.57% | 52.25%

9.4 | 060 | 3.73% | 52.06%

11.0 | 070 | 4.36% | 52.34%

1000.0

1.9 | 010 | 0.42% | 50.72%

4.1 | 020 | 2.21% | 51.68%

5.8 | 030 | 3.25% | 52.12%

7.3 | 040 | 2.69% | 51.66%

8.8 | 050 | 3.57% | 52.25%

10.3 | 060 | 3.73% | 52.06%

12.0 | 070 | 4.36% | 52.34%

10000.0

1.8 | 010 | 0.42% | 50.72%

3.4 | 020 | 2.21% | 51.68%

4.8 | 030 | 3.25% | 52.12%

6.0 | 040 | 2.69% | 51.66%

7.6 | 050 | 3.57% | 52.25%

8.8 | 060 | 3.73% | 52.06%

10.2 | 070 | 4.36% | 52.34%

100000.0

1.8 | 010 | 0.42% | 50.72%

3.4 | 020 | 2.21% | 51.68%

4.9 | 030 | 3.25% | 52.12%

6.4 | 040 | 2.69% | 51.66%

7.8 | 050 | 3.57% | 52.25%

9.3 | 060 | 3.73% | 52.06%

10.7 | 070 | 4.36% | 52.34%四、Evaluate Results 评估结果

python

log_scores = pd.DataFrame(log_scores, columns=cols)

log_scores.to_hdf('data.h5', 'logistic/scores')

log_coeffs = pd.DataFrame(log_coeffs, index=X.columns).T

log_coeffs.to_hdf('data.h5', 'logistic/coeffs')

log_predictions = pd.concat(log_predictions)

log_predictions.to_hdf('data.h5', 'logistic/predictions')

log_scores = pd.read_hdf('data.h5', 'logistic/scores')

log_scores.info()

log_scores.groupby('C').auc.describe()

| | count | mean | std | min | 25% | 50% | 75% | max |

| C | | | | | | | | |

| 0.00001 | 75.0 | 0.524834 | 0.033162 | 0.462730 | 0.500238 | 0.520174 | 0.543183 | 0.608531 |

| 0.00010 | 75.0 | 0.525391 | 0.033182 | 0.465664 | 0.500457 | 0.520052 | 0.539332 | 0.617832 |

| 0.00100 | 75.0 | 0.525726 | 0.034815 | 0.442510 | 0.499963 | 0.521454 | 0.546595 | 0.637523 |

| 0.01000 | 75.0 | 0.525146 | 0.036003 | 0.447376 | 0.500513 | 0.519809 | 0.547387 | 0.633047 |

| 0.10000 | 75.0 | 0.523507 | 0.036001 | 0.439579 | 0.501279 | 0.517053 | 0.548712 | 0.617858 |

| 1.00000 | 75.0 | 0.523068 | 0.035935 | 0.438185 | 0.500740 | 0.516178 | 0.548256 | 0.614613 |

| 10.00000 | 75.0 | 0.523020 | 0.035928 | 0.438122 | 0.500564 | 0.516100 | 0.548231 | 0.614639 |

| 100.00000 | 75.0 | 0.523012 | 0.035928 | 0.438088 | 0.500543 | 0.516050 | 0.548237 | 0.614629 |

| 1000.00000 | 75.0 | 0.523011 | 0.035929 | 0.438074 | 0.500541 | 0.516038 | 0.548239 | 0.614629 |

| 10000.00000 | 75.0 | 0.523010 | 0.035929 | 0.438079 | 0.500541 | 0.516038 | 0.548239 | 0.614629 |

| 100000.00000 | 75.0 | 0.523010 | 0.035929 | 0.438079 | 0.500541 | 0.516038 | 0.548239 | 0.614629 |

|---|

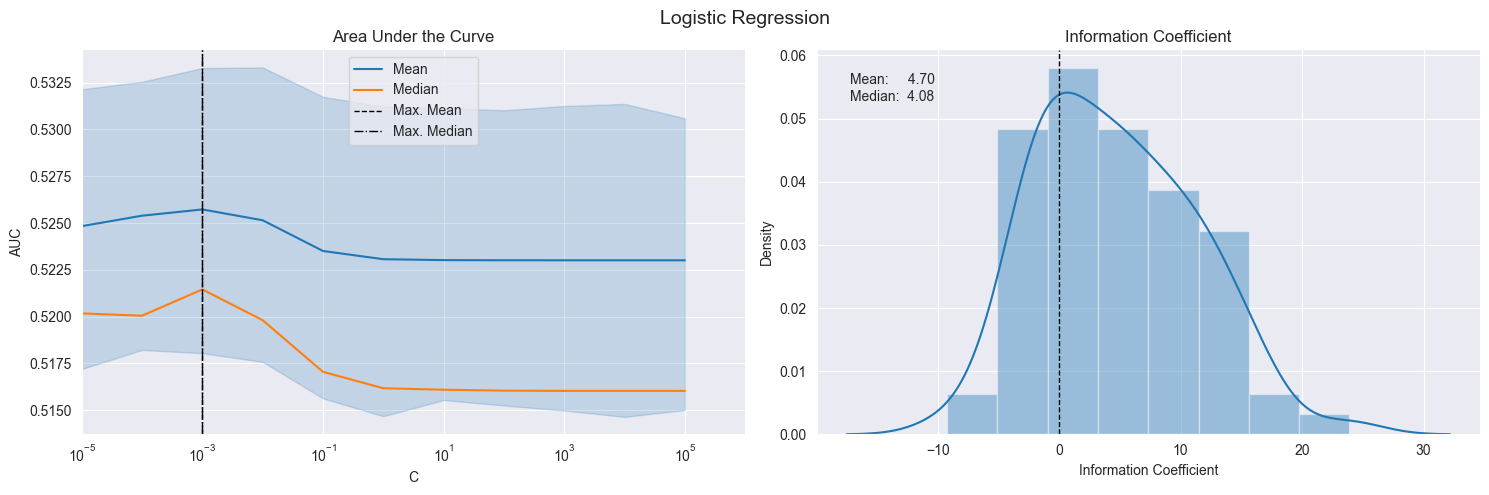

五、Plot Validation Scores 绘制验证分数

python

def plot_ic_distribution(df, ax=None):

if ax is not None:

sns.distplot(df.ic, ax=ax)

else:

ax = sns.distplot(df.ic)

mean, median = df.ic.mean(), df.ic.median()

ax.axvline(0, lw=1, ls='--', c='k')

ax.text(x=.05, y=.9, s=f'Mean: {mean:8.2f}\nMedian: {median:5.2f}',

horizontalalignment='left',

verticalalignment='center',

transform=ax.transAxes)

ax.set_xlabel('Information Coefficient')

sns.despine()

plt.tight_layout()

fig, axes= plt.subplots(ncols=2, figsize=(15, 5))

sns.lineplot(x='C', y='auc', data=log_scores, estimator=np.mean, label='Mean', ax=axes[0])

by_alpha = log_scores.groupby('C').auc.agg(['mean', 'median'])

best_auc = by_alpha['mean'].idxmax()

by_alpha['median'].plot(logx=True, ax=axes[0], label='Median', xlim=(10e-6, 10e5))

axes[0].axvline(best_auc, ls='--', c='k', lw=1, label='Max. Mean')

axes[0].axvline(by_alpha['median'].idxmax(), ls='-.', c='k', lw=1, label='Max. Median')

axes[0].legend()

axes[0].set_ylabel('AUC')

axes[0].set_xscale('log')

axes[0].set_title('Area Under the Curve')

plot_ic_distribution(log_scores[log_scores.C==best_auc], ax=axes[1])

axes[1].set_title('Information Coefficient')

fig.suptitle('Logistic Regression', fontsize=14)

sns.despine()

fig.tight_layout()

fig.subplots_adjust(top=.9);