Python金融入门

- [1. 加载数据与可视化](#1. 加载数据与可视化)

-

- [1.1. 加载数据](#1.1. 加载数据)

- [1.2. 折线图](#1.2. 折线图)

- [1.3. 重采样](#1.3. 重采样)

- [1.4. K线图 / 蜡烛图](#1.4. K线图 / 蜡烛图)

- [1.5. 挑战1](#1.5. 挑战1)

- [2. 计算](#2. 计算)

-

- [2.1. 收益 / 回报](#2.1. 收益 / 回报)

- [2.2. 绘制收益图](#2.2. 绘制收益图)

- [2.3. 累积收益](#2.3. 累积收益)

- [2.4. 波动率](#2.4. 波动率)

- [2.5. 挑战2](#2.5. 挑战2)

- [3. 滚动窗口](#3. 滚动窗口)

-

- [3.1. 创建移动平均线](#3.1. 创建移动平均线)

- [3.2. 绘制移动平均线](#3.2. 绘制移动平均线)

- [3.3 Challenge](#3.3 Challenge)

- [4. 技术分析](#4. 技术分析)

-

- [4.1. OBV](#4.1. OBV)

- [4.2. 累积/派发指标(A/D)](#4.2. 累积/派发指标(A/D))

- [4.3. RSI](#4.3. RSI)

1. 加载数据与可视化

1.1. 加载数据

python

# 导入所需库

from matplotlib import dates

import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

import yfinance as yf

python

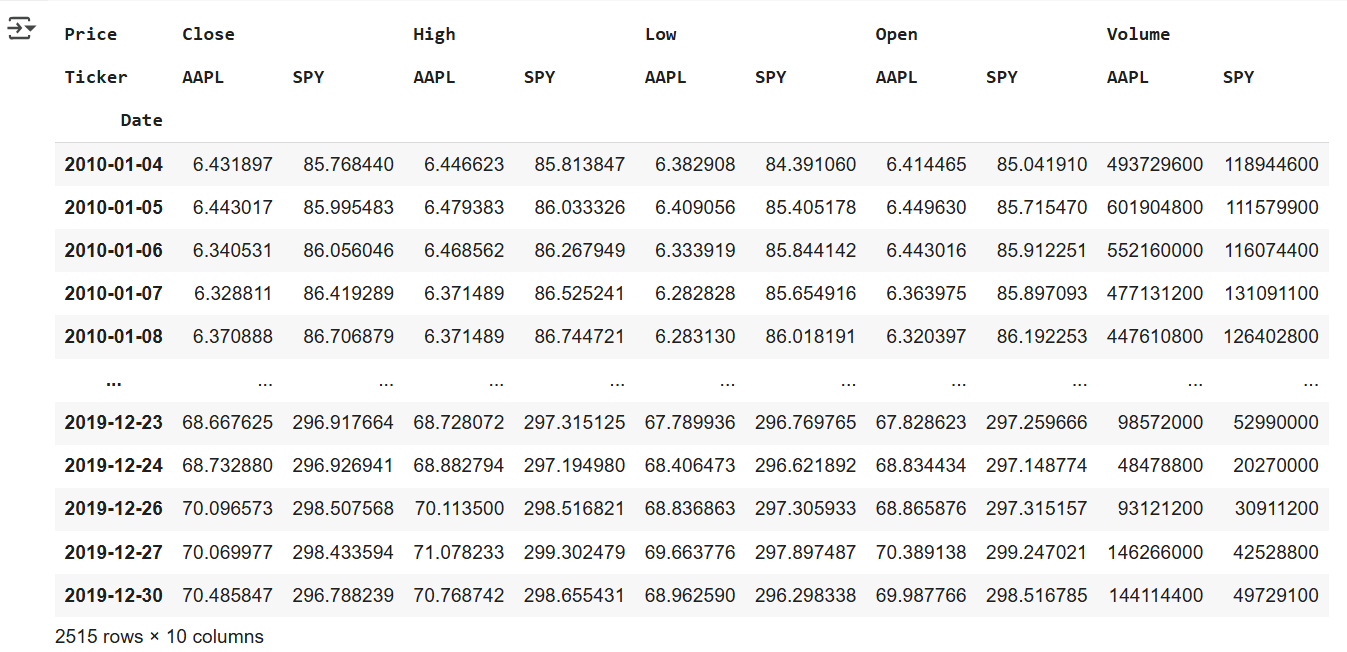

# 使用Y Finance库下载S&P500数据以及2010年至2019年底的Apple数据

raw = yf.download('SPY AAPL', start='2010-01-01', end='2019-12-31')

python

raw

# Y Finance使用日期作为索引列, 每行代表一天。

# 查看列:这里有所谓的分层或多索引列,可以看到调整后的收盘价,因为我们同时要求苹果和标准普尔 500指数

# 所以我们在它下面有两个子列,可以看到收盘价、最高值、最低值、开盘价、 和Volumn

python

# 检查数据帧的columns属性

raw.columns

python

# 查看pipe的用法

raw.pipe?

python

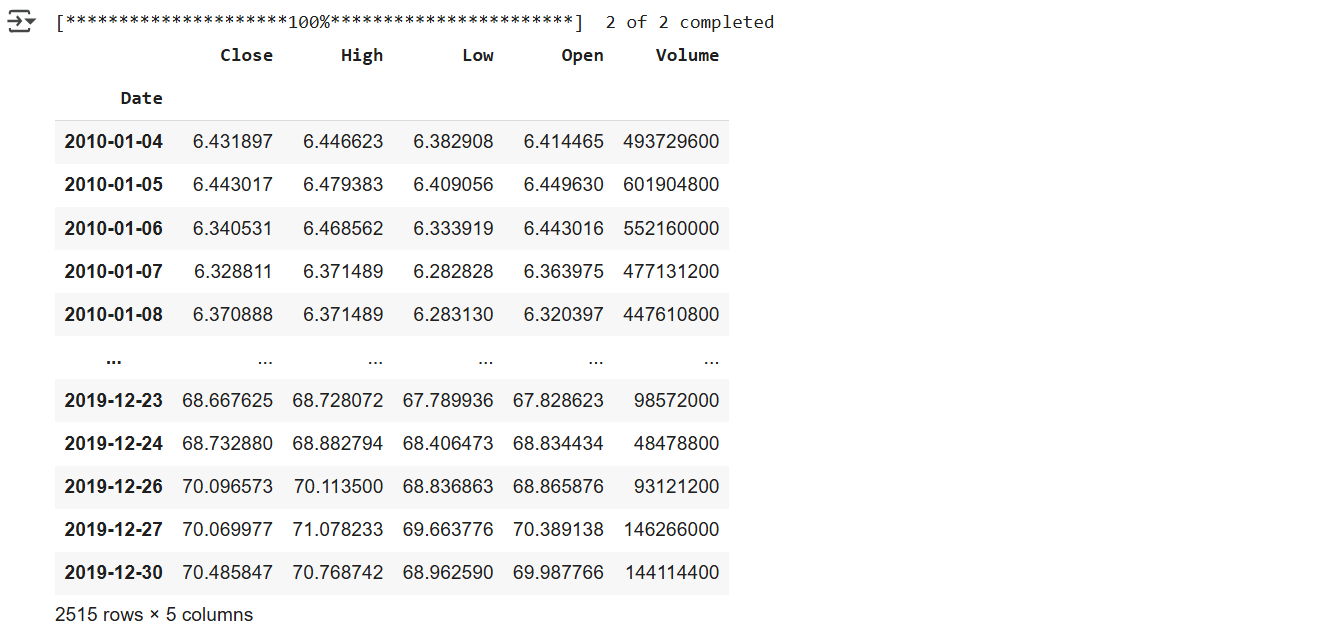

import yfinance as yf

#fix_cols():重命名多层列索引为单层(只保留子列名)

def fix_cols(df):

columns = df.columns

outer = [col[0] for col in columns]

df.columns = outer

return df

# 加载与清洗逻辑封装在一个函数里,便于复用

def tweak_data():

raw = yf.download('SPY AAPL',start='2010-01-01', end='2019-12-31')

return (raw

.iloc[:,::2]

.pipe(fix_cols)) # pipe():在链式调用中插入一个自定义函数。

tweak_data()

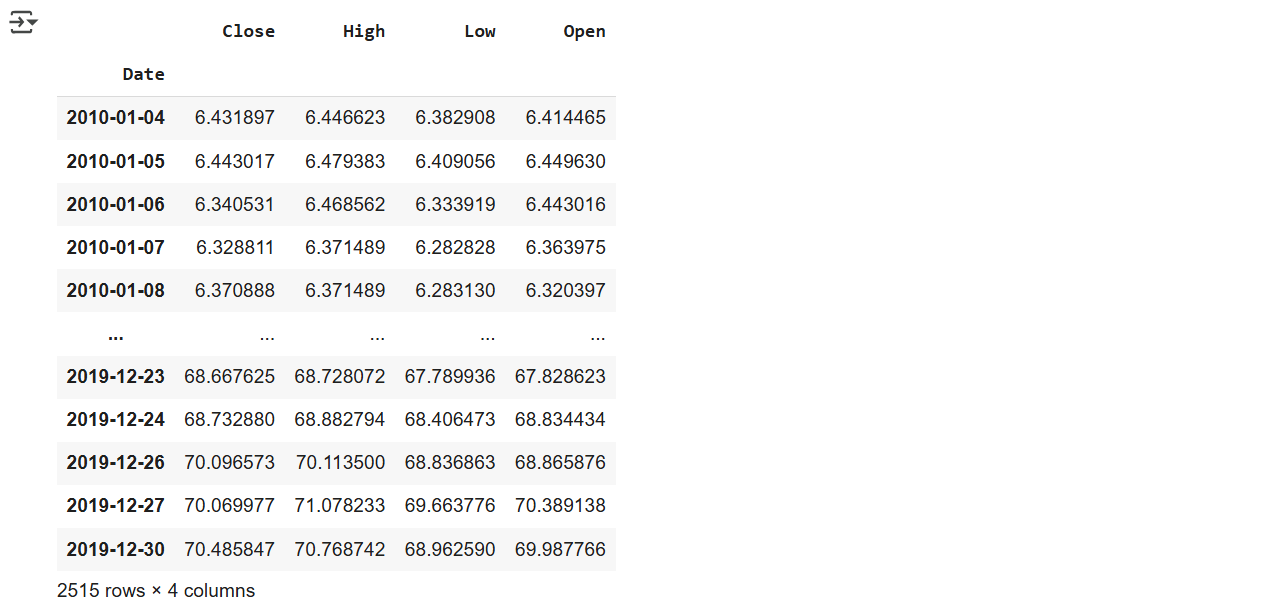

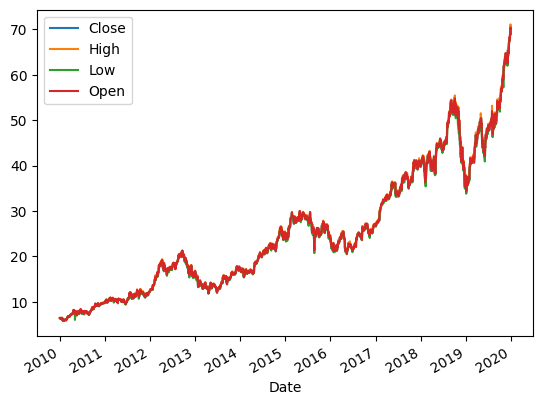

1.2. 折线图

创建线图,并整绘图的细节(如选择列、大小等)。

python

(raw

.iloc[:,:-2:2] #从第0列开始,到倒数第2列,步长为2

.pipe(fix_cols)

)

python

(raw

.iloc[:,:-2:2]

.pipe(fix_cols)

.plot()

)

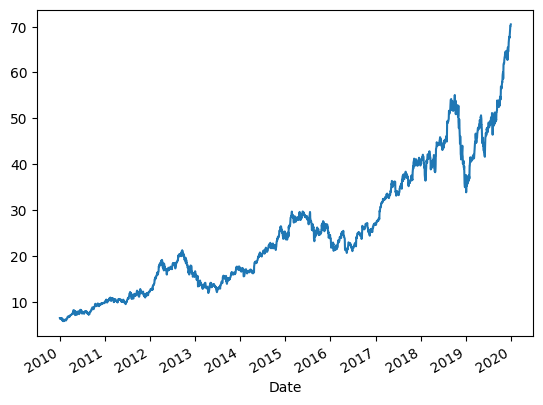

python

(raw

.iloc[:,:-2:2]

.pipe(fix_cols)

.Close

.plot()

)

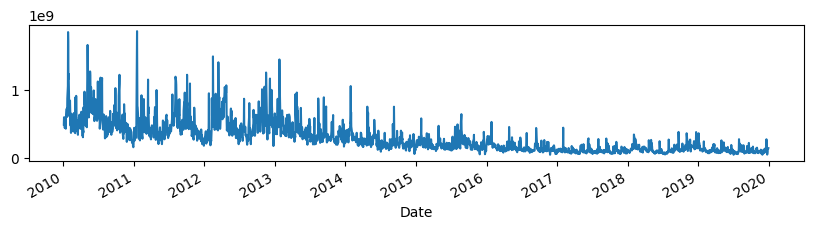

python

(raw

.iloc[:,::2]

.pipe(fix_cols)

.Volume

.plot(figsize=(10,2)) # 10英寸宽,2英寸高

)

1.3. 重采样

重新采样(resampling) 是将时间序列数据的频率从一个粒度转换为另一个粒度的过程,如从每日 → 每月,Pandas 提供了.resample() 方法。

python

(raw

.iloc[:,::2]

.pipe(fix_cols)

.Close # 每日收盘价

.plot()

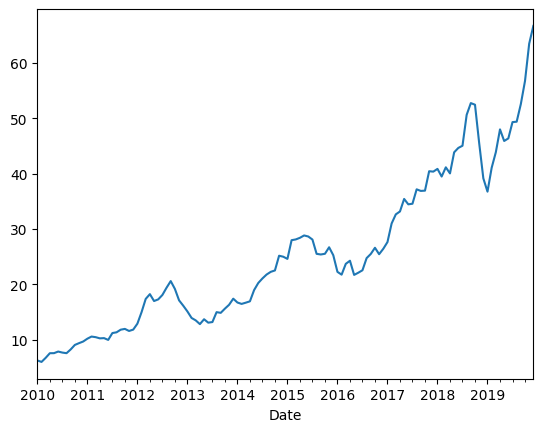

)按月份分组:

python

(raw

.iloc[:,::2]

.pipe(fix_cols)

.resample('M') # offset alias

.Close

)

python

(raw

.iloc[:,::2]

.pipe(fix_cols)

.resample('M') # offset alias

.Close

.mean()

.plot() # 索引中有日期,列中有值,这样就可以绘制了

)

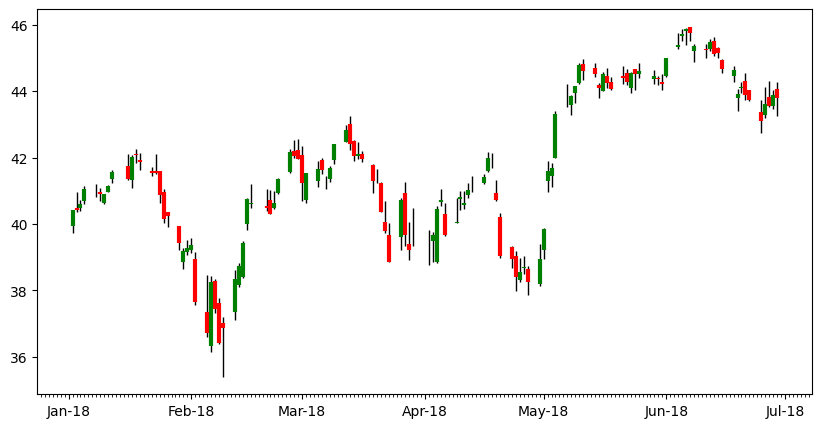

1.4. K线图 / 蜡烛图

python

fig, ax = plt.subplots(figsize=(10,5))

def plot_candle(df, ax):

# wick

ax.vlines(x=df.index, ymin=df.Low, ymax=df.High, colors='k', linewidth=1)

# red - decrease

red = df.query('Open > Close')

ax.vlines(x=red.index, ymin=red.Close, ymax=red.Open, colors='r', linewidth=3)

# green - increase

green = df.query('Open <= Close')

ax.vlines(x=green.index, ymin=green.Close, ymax=green.Open, colors='g', linewidth=3)

ax.xaxis.set_major_locator(dates.MonthLocator())

ax.xaxis.set_major_formatter(dates.DateFormatter('%b-%y'))

ax.xaxis.set_minor_locator(dates.DayLocator())

return df

(raw

.iloc[:,::2]

.pipe(fix_cols)

.resample('d')

.agg({'Open':'first', 'High':'max', 'Low':'min', 'Close':'last'})

.loc['jan 2018':'jun 2018']

.pipe(plot_candle, ax)

)

1.5. 挑战1

Plot the candles for the time period of Sep 2019 to Dec 2019. 可以做做看

2. 计算

Goal

- Explore Pandas methods like

.pct_change - Plotting with Pandas

- Refactoring to functions

2.1. 收益 / 回报

在金融中,"回报"通常指某个资产价格在两个时间点之间的相对变化。在Pandas中使用.pct_change() 方法计算百分比变化(Percentage Change),默认按前一行计算百分比变化(periods=1)。

python

# 使用aapl存储

aapl = (raw

.iloc[:,::2]

.pipe(fix_cols)

)

aapl

python

# returns

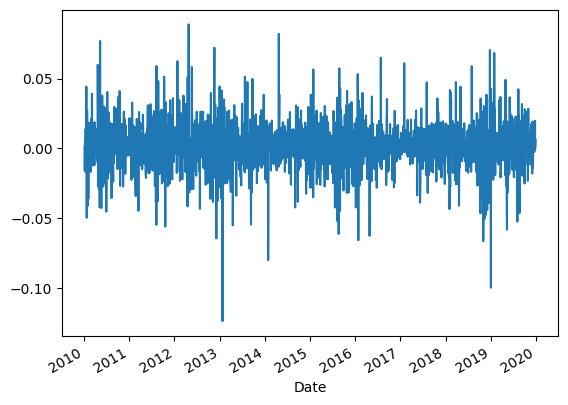

aapl.pct_change()2.2. 绘制收益图

使用 .plot() 方法,查看回报的日常变化趋势。

python

# plot returns

(aapl

.pct_change()

.Close

.plot()

)很多高频噪声,看起来像"毛毛虫":

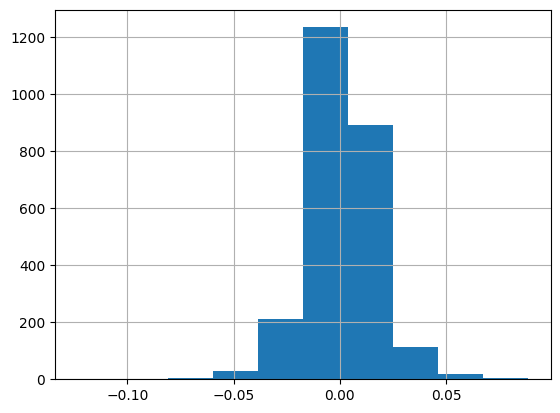

使用 .hist() 方法来观察回报的 分布情况(正负、极值、对称性等)。

python

# Histogram of Returns

(aapl

.pct_change()

.Close

.hist()

)

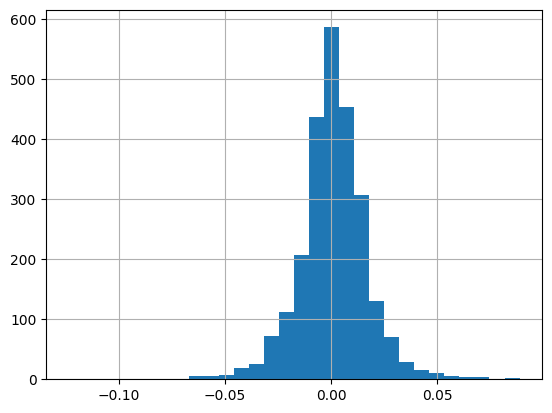

bins=30 表示分成 30 个区间,可以更细致地看到分布:

python

# Change bins

(aapl

.pct_change()

.Close

.hist(bins=30)

)

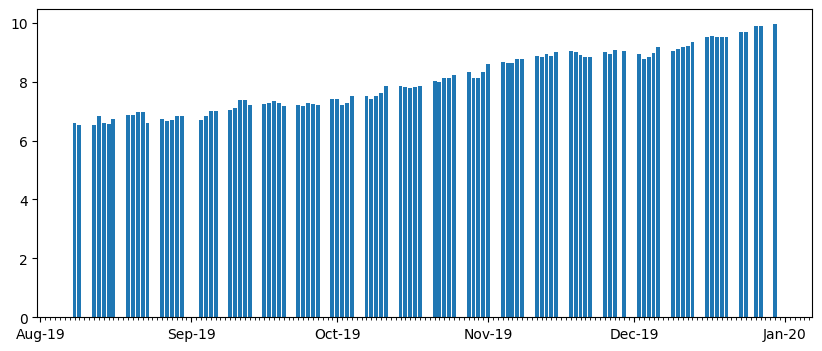

条形图用于查看一小段时间内每日的正负回报(比如最近 100 天):

python

# Understanding plotting in Pandas is a huge lever

# Bar Plot Returns

(aapl

.pct_change()

.Close

.iloc[-100:] # 获取最后100个值

.plot.bar()

)Pandas 会把日期索引变成"分类变量",导致 X 轴标签重叠、无法格式化。

即使调整标签,也会显示成 1970-01 等错误日期:

python

# Bar Plot of Returns

# Sadly dates are broken with Pandas bar plots

# 1970s?

fig, ax = plt.subplots(figsize=(10, 4))

(aapl

.pct_change()

.Close

.iloc[-100:]

.plot.bar(ax=ax)

)

ax.xaxis.set_major_locator(dates.MonthLocator())

ax.xaxis.set_major_formatter(dates.DateFormatter('%b-%y'))

ax.xaxis.set_minor_locator(dates.DayLocator())

解决办法:使用 Matplotlib 手动绘制条形图

python

# Returns - using matplotlib

def my_bar(ser, ax):

ax.bar(ser.index, ser)

ax.xaxis.set_major_locator(dates.MonthLocator())

ax.xaxis.set_major_formatter(dates.DateFormatter('%b-%y'))

ax.xaxis.set_minor_locator(dates.DayLocator())

return ser

fig, ax = plt.subplots(figsize=(10, 4))

_ = (aapl

.pct_change()

.Close

.iloc[-100:]

.pipe(my_bar, ax)

)

2.3. 累积收益

Goal:

- More complicated Pandas

- Refactoring into a function

- Explore source

- Creating new columns with

.assign - Illustrate lambda

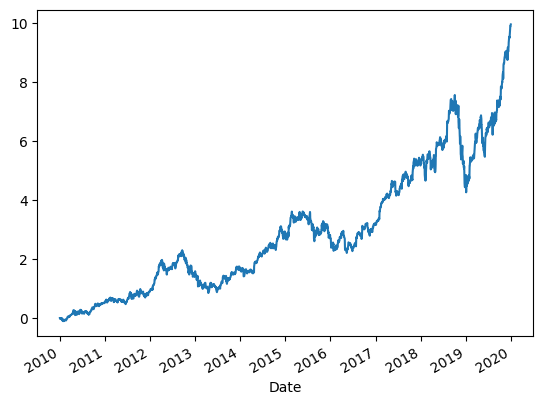

Cumulative Returns is the amount that investment has gained or lost over time:

(current_price-original_price)/original_price

python

(aapl

.Close

.plot()

)逐步计算:

python

(aapl

.Close

.sub(aapl.Close[0]) # substract

.div(aapl.Close[0]) # divide

.plot()

)基于日收益的累积积:

python

# alternatte calculation

(aapl

.Close # 取出收盘价序列

.pct_change() # 计算日收益率(百分比变化)

.add(1) # 转换为收益倍率 (1 + r)

.cumprod() # 计算累积乘积:累计收益倍率

.sub(1) # 转换为累计收益率:累计倍率 - 1

.plot() # 绘图

) 函数化重构:

python

# create a function for calculating

def calc_cum_returns(df,col):

ser = df[col]

return (ser

.sub(ser[0])

.div(ser[0]))

(aapl

.pipe(calc_cum_returns,'Close')

.plot()

)

python

# Lambda is an *anonymous function*

def get_returns(df):

return calc_cum_returns(df,'Close')

get_returns(aapl)lambda这里我不太明白

python

(lambda df: get_returns(df))(aapl)

python

# Create a new column

(aapl

.assign(cum_returns=lambda df: calc_cum_returns(df,'Close'))

)

python

# Returns - using matplotlib

def my_bar(ser, ax):

ax.bar(ser.index, ser)

ax.xaxis.set_major_locator(dates.MonthLocator())

ax.xaxis.set_major_formatter(dates.DateFormatter('%b-%y'))

ax.xaxis.set_minor_locator(dates.DayLocator())

return ser

fig, ax = plt.subplots(figsize=(10, 4))

_ = (aapl

.pipe(calc_cum_returns, 'Close')

.iloc[-100:]

.pipe(my_bar, ax)

)

2.4. 波动率

Goals

- More complicated Pandas

- Learn about rolling operations

波动性(英语:volatility,又称波动率),指金融资产在一定时间段的变化性。在股票市场,以每天收市价计算的波动性称为历史波幅(Historical Volatility),以股票期权估算的未来波动性称为引申波幅(Implied Volatility)。着名的VIX指数是标准普尔500指数期权的30日引申波幅,以年度化表示。(维基百科)

python

(aapl

.Close

.mean()

)

python

(aapl

.Close

.std()

)

python

(aapl

.assign(pct_change_close=aapl.Close.pct_change())

.pct_change_close

.std()

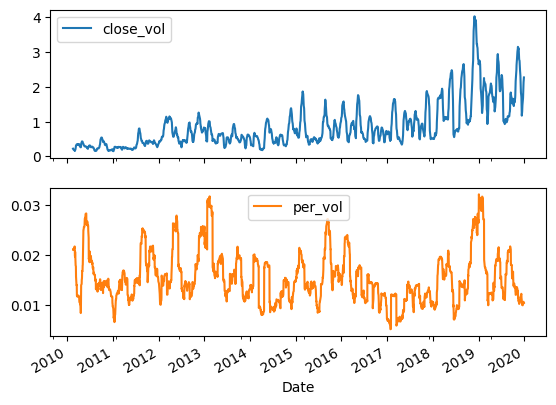

)以滑动窗口方式计算"过去 N 天"的波动性:

python

(aapl

.assign(close_vol=aapl.rolling(30).Close.std(),

per_vol=aapl.Close.pct_change().rolling(30).std())

.iloc[:,-2:]

.plot(subplots=True)

)

以固定周期(如每 15 天)进行分组计算标准差:

python

# 15 day volatility

(aapl

.assign(pct_change_close=aapl.Close.pct_change()) # 创建一个名为百分比变化的列

.resample('15D') # 15天为一个分组

.std()

)

python

# 15 day rolling volatility

(aapl

.assign(pct_change_close=aapl.Close.pct_change()) # 创建一个名为百分比变化的列

.rolling(window=15, min_periods=15)

.std()

)

python

# 15 day volatility

# note if column name conflicts with method need to use

# index access ([])

(aapl

.assign(pct_change=aapl.Close.pct_change())

.rolling(window=15, min_periods=15)

.std()

['pct_change']

.plot()

)

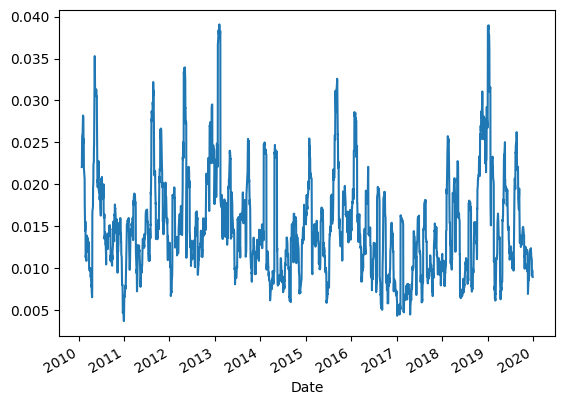

2.5. 挑战2

Plot the rolling volatility over 30-day sliding windows for 2015-2019。(可以参考上面的代码)

3. 滚动窗口

3.1. 创建移动平均线

对苹果公司股票(aapl)的价格数据进行三日移动平均(ma3)的计算:

python

(aapl

.assign(s1=aapl.Close.shift(1),

s2=aapl.Close.shift(2),

ma3=lambda df_:df_.loc[:, ['Close', 's1', 's2']].mean(axis='columns'),

ma3_builtin=aapl.Close.rolling(3).mean()

)

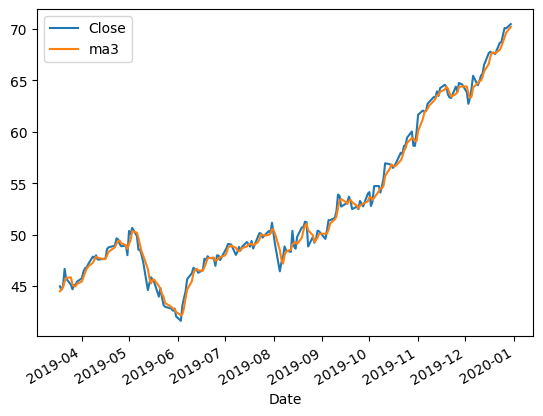

)3.2. 绘制移动平均线

python

(aapl

.assign(s1=aapl.Close.shift(1),

s2=aapl.Close.shift(2),

ma3=lambda df_:df_.loc[:, ['Close', 's1', 's2']].mean(axis='columns'),

ma3_builtin=aapl.Close.rolling(3).mean()

)

[['Close','ma3']]

.iloc[-200:]

.plot()

)

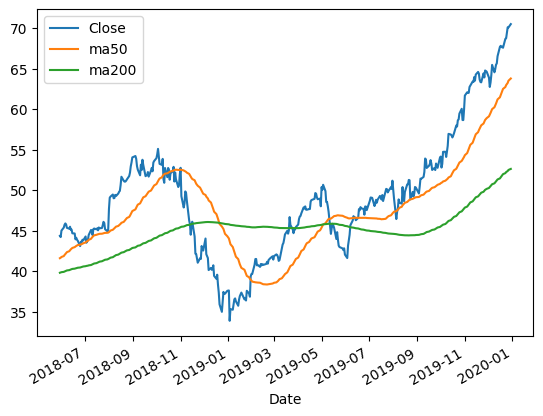

可视化苹果公司股票的收盘价与其 50 日、200 日移动平均线(MA):

python

(aapl

.assign(

ma50=aapl.Close.rolling(50).mean(),

ma200=aapl.Close.rolling(200).mean(),

)

[['Close', 'ma50', 'ma200']]

.iloc[-400:]

.plot()

)如下图可以看到:Close(原始收盘价)是日常波动最明显的一条线;ma50是比较敏感的短期趋势线;而ma200是更平滑的长期趋势线。

3.3 Challenge

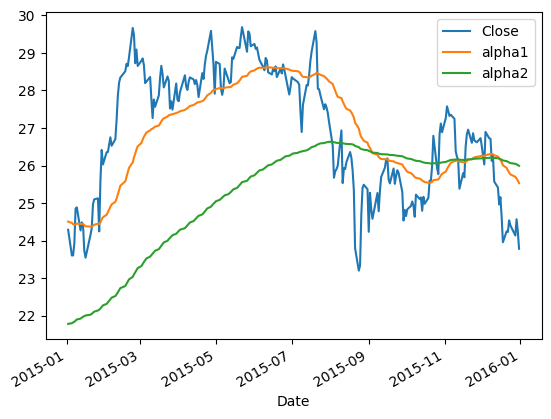

Create a plot with three lines:

- AAPL close price in 2015

- Exponential moving average with alpha =. 0392

- Exponential moving average with alpha =. 00995

Hint:Use the .ewm method to create a rolling aggregator.

python

aapl.ewm?

python

(aapl

.loc['2015']

.assign(

alpha1=aapl.Close.ewm(alpha=0.0392).mean(),

alpha2=aapl.Close.ewm(alpha=0.00995).mean(),

)

[['Close', 'alpha1', 'alpha2']]

.plot()

)alpha=0.0392:较高,表示更敏感,近期数据权重大,从而曲线更贴近原始价格;alpha=0.00995:较低,更平滑,趋势线更慢反应价格波动。

4. 技术分析

4.1. OBV

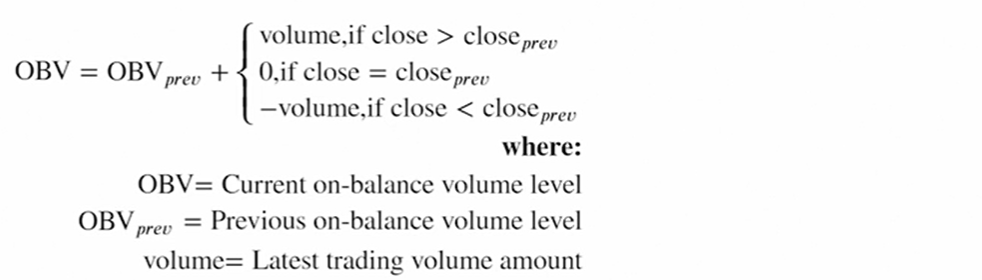

OBV(On-Balance Volume,能量潮指标),是一种常见的技术分析指标,用来结合价格走势和成交量判断趋势强度。OBV 是一个累加值:如果今日收盘价 > 昨日 → 当日成交量加到 OBV 上;如果今日收盘价 < 昨日 → 当日成交量从 OBV 中减去;如果收盘价不变 → OBV 保持不变,如下图:

下面函数的实现逻辑是对的,但是效率不高,会触发FutureWarning:

python

# naive

def calc_obv(df):

df = df.copy()

df["OBV"] = 0.0

# Loop through the data and calculate OBV

for i in range(1, len(df)):

# 如果该仓位的收盘价大于前一个收盘值

if df["Close"][i] > df["Close"][i - 1]:

df["OBV"][i]=df["OBV"][i - 1] + df["Volume"][i]

elif df["Close"][i] < df["Close"][i - 1]:

df["OBV"][i]=df["OBV"][i -1]-df["Volume"][i]

else:

df["OBV"][i] = df["OBV"][i - 1]

return df

calc_obv(aapl)用 Pandas 向量化方式计算 OBV并使用 %timeit 测试:

python

%%timeit

# This is painful

(aapl

.assign(close_prev=aapl.Close.shift(1),

vol=0,

obv=lambda adf: adf.vol.where(cond=adf.Close == adf.close_prev,

other=adf.Volume.where(cond=adf.Close > adf.close_prev,

other =- adf.Volume.where(cond=adf.Close < adf.close_prev, other=0)

)).cumsum()

)

)用 np.select 实现 OBV 的向量化计算:

python

(aapl

.assign(prev_close=aapl.Close.shift(1),

vol=np.select([aapl.Close> aapl.Close.shift(1),

aapl.Close == aapl.Close.shift(1),

aapl.Close < aapl.Close.shift(1)],

[aapl.Volume, 0, -aapl.Volume]),

obv=lambda df_:df_. vol.cumsum(),

)

)将 OBV 的向量化计算封装成函数 calc_obv():

python

def calc_obv(df, close_col='Close', vol_col='Volume'):

close = df[close_col]

vol = df[vol_col]

close_shift = close.shift(1)

return (df

.assign(vol=np.select([close > close_shift,

close == close_shift,

close < close_shift],

[vol, 0, -vol]),

obv=lambda df_:df_. vol.fillna(0).cumsum()

)

['obv']

)

(aapl

.assign(obv=calc_obv)

)4.2. 累积/派发指标(A/D)

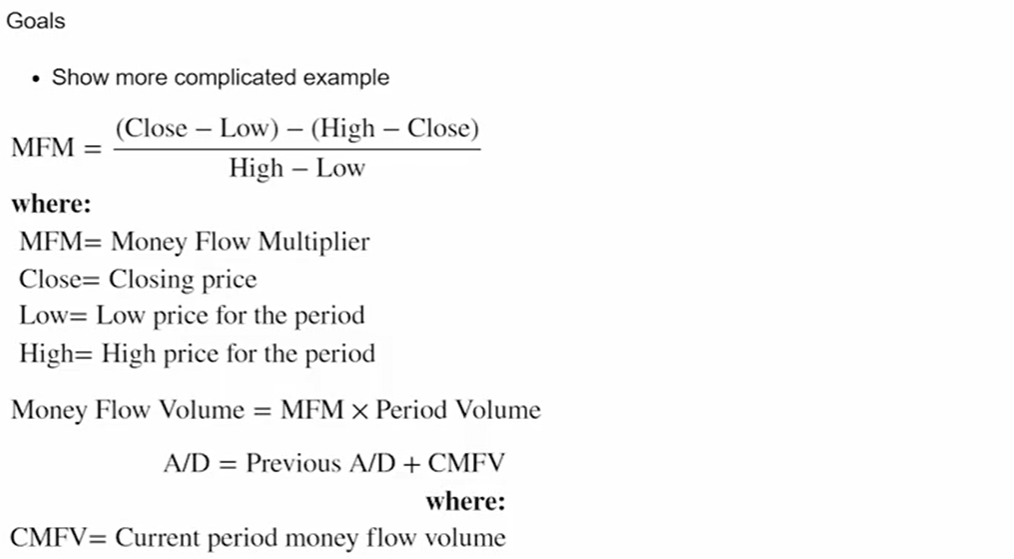

A/D 指标(Accumulation/Distribution Line,累积/派发线)是技术分析中衡量资金流入流出的常用指标之一。

- MFM(Money Flow Multiplier):资金流动乘数,用于衡量收盘价相对当天价格区间的位置,范围在-1, 1,越接近 1 表示更靠近高点(资金流入),越接近 -1 表示更靠近低点(资金流出)。

- Money Flow Volume(资金流动量):把价格位置信息与成交量结合起来,收盘越靠近高点,且成交量越大,说明有更多资金"流入"。

- A/D 是一个累计值,用来判断市场是否处于吸筹(Accumulation)还是派发(Distribution)。

实现逻辑:

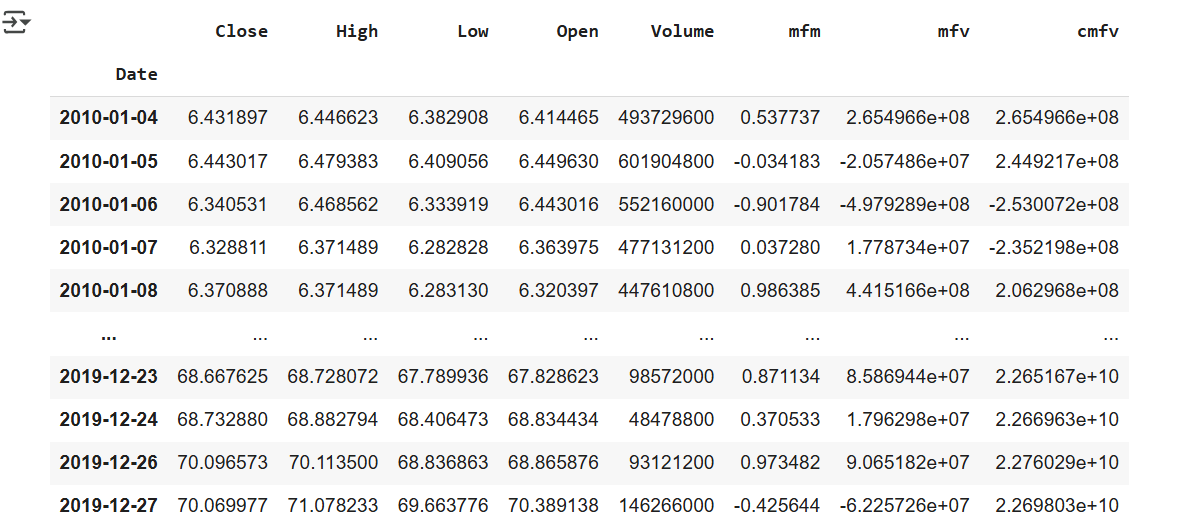

python

(aapl

.assign(mfm=((aapl.Close - aapl.Low) - (aapl.High - aapl.Close))/(aapl.High - aapl.Low),

mfv=lambda df_:df_.mfm * df_.Volume, # lambda将采用数据帧的当前值

cmfv=lambda df_:df_.mfv.cumsum()

)

)

python

# 重构为一个函数

def calc_ad(df, close_col='Close', low_col='Low', high_col='High',vol_col='Volume'):

close = df[close_col]

low = df[low_col]

high = df[high_col]

return (df

.assign(mfm=((close - low) -(high - close))/(high - low),

mfv=lambda df_: df_. mfm * df_[vol_col],

cmfv=lambda df_: df_. mfv.cumsum())

.cmfv

)

(aapl

.assign(ad=calc_ad)

.ad

.plot()

)!在这里插入图片描述(https://i-blog.csdnimg.cn/direct/9b0a4fe5d9624d968f56b97b499d801c.png

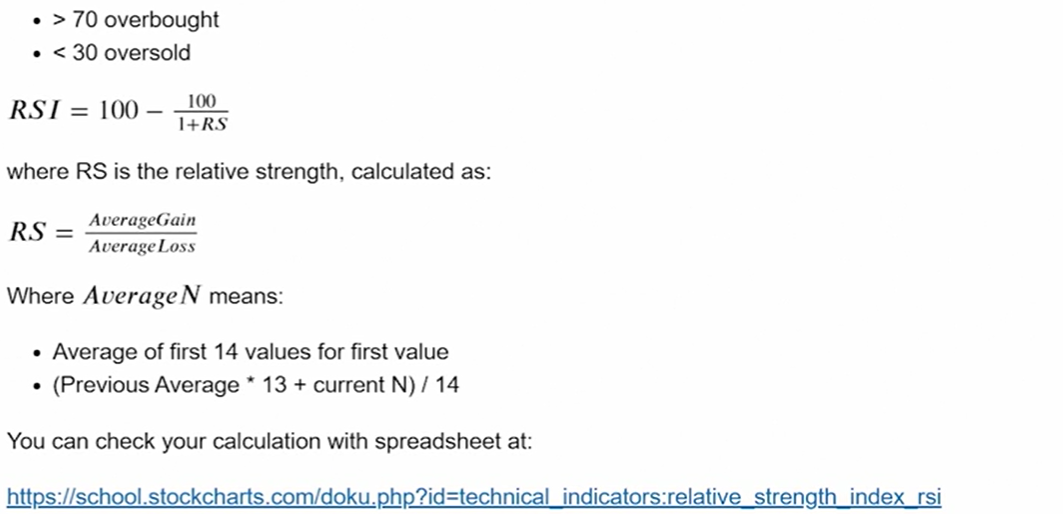

4.3. RSI

Create code to create an Relative Strength Income(RSI) column. Relative Strength Index is a popular momentum indicator

RSI(Relative Strength Index, 相对强弱指数)是一种常用的技术分析指标,用于衡量股票或其他资产价格的近期涨跌强度,帮助判断市场是否处于超买或超卖状态。RSI 的应用意义:

- 超买区:RSI 通常高于 70,意味着价格上涨过快,可能出现回调。

- 超卖区:RSI 通常低于 30,意味着价格下跌过快,可能出现反弹。

- 趋势判断:RSI 可以帮助确认价格趋势的强度和反转信号。

python

(aapl

.assign(mfm=((aapl.Close - aapl.Low) - (aapl.High - aapl.Close))/(aapl.High - aapl.Low),

mfv=lambda df_:df_.mfm * df_.Volume, # lambda将采用数据帧的当前值

cmfv=lambda df_:df_.mfv.cumsum()

)

)

python

# prompt: Create 14-day RSI column

def rsi(df: pd.DataFrame, window: int = 14) -> pd.DataFrame:

"""

Calculates the Relative Strength Index (RSI) for a given DataFrame.

Args:

df: The input DataFrame with a 'Close' column.

window: The lookback window for RSI calculation (default is 14).

Returns:

The DataFrame with an added 'RSI' column.

"""

delta = df['Close'].diff()

up, down = delta.copy(), delta.copy()

up[up < 0] = 0

down[down > 0] = 0

# Use rolling mean

avg_gain = up.rolling(window=window).mean()

avg_loss = abs(down.rolling(window=window).mean())

rs = avg_gain / avg_loss

df['RSI'] = 100 - (100 / (1 + rs))

return df.RSI

# aapl = rsi(aapl)

# print(aapl.head(16))

(aapl

.assign(rsi_14=rsi(aapl))

.rsi_14

# .plot()

)