引言

"我们的推荐系统准确率又提升了5%!"------但你知道用户点击增加是因为推荐本身,还是因为同时进行的营销活动?这种"混淆变量"的陷阱,正是传统机器学习无法跨越的鸿沟。

开篇:相关性≠因果性------机器学习的"认知革命"

如果你在入门和进阶阶段已经掌握了如何让模型"预测准确",那今天这篇将带你进入一个更深刻的领域:让模型理解世界 ,而不只是拟合数据。

想象这样一个场景:你的电商平台数据显示,买尿布的顾客也常买啤酒 。传统机器学习会兴奋地告诉你:"快把啤酒放在尿布旁边!"。但如果你深入思考,可能会发现一个被忽略的第三变量 :深夜购物的年轻爸爸。他们既要买尿布,也想买啤酒放松------这才是真正的因果链条。

这就是传统机器学习的盲点 :它只看到相关性 ,却无法理解因果性。而今天我们要探讨的三个前沿方向------因果机器学习、可解释AI、科学智能------正是要让AI从"数据拟合器"进化为"世界理解者"。

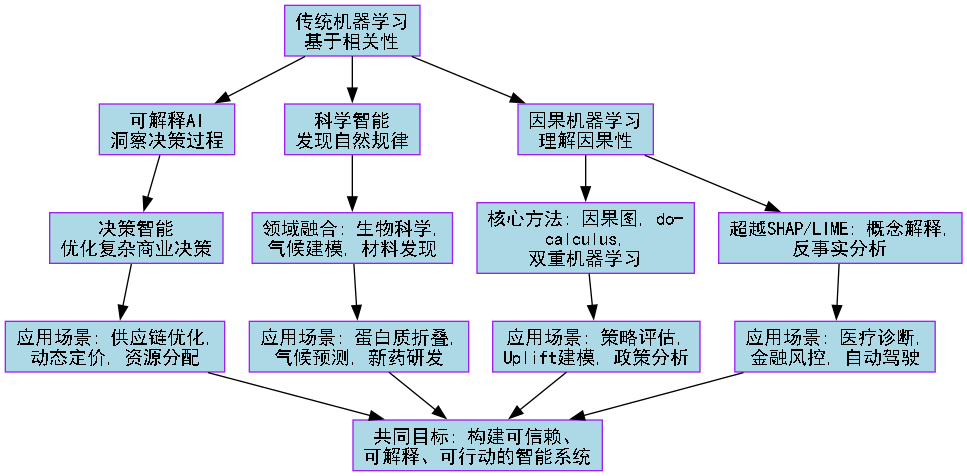

为了让这次探索之旅更加清晰,我们先来看一张全景地图,它展示了从传统机器学习到前沿智能的认知升级路径:

理解了这个认知升级的框架,我们就正式开始这次前沿探索之旅。第一站,我们将挑战机器学习最根本的假设:相关性是否足够?

第一部分:因果机器学习------让AI学会"反事实思考"

从辛普森悖论说起:为什么数据会"说谎"?

1973年,加州大学伯克利分校被指控性别歧视:研究生院整体录取数据显示,男性的录取率(44%)明显高于女性(35%) 。但当人们按院系细分数据后,却发现了一个诡异现象:几乎每个院系女性的录取率都高于或等于男性。

这就是著名的辛普森悖论:整体趋势与分组趋势完全相反。原因何在?女性更多申请了录取率低的院系(如物理、数学),而男性更多申请了录取率高的院系(如教育、艺术)。

传统机器学习会得出什么结论?

-

只看整体数据:性别歧视存在!

-

深入看分组数据:没有歧视,甚至略有优势

但因果机器学习会问更深的问题:

-

为什么女性更倾向申请难录取的院系?

-

录取率差异是院系选择导致的,还是录取过程本身?

-

如果改变申请策略,会发生什么?

因果革命的三把钥匙

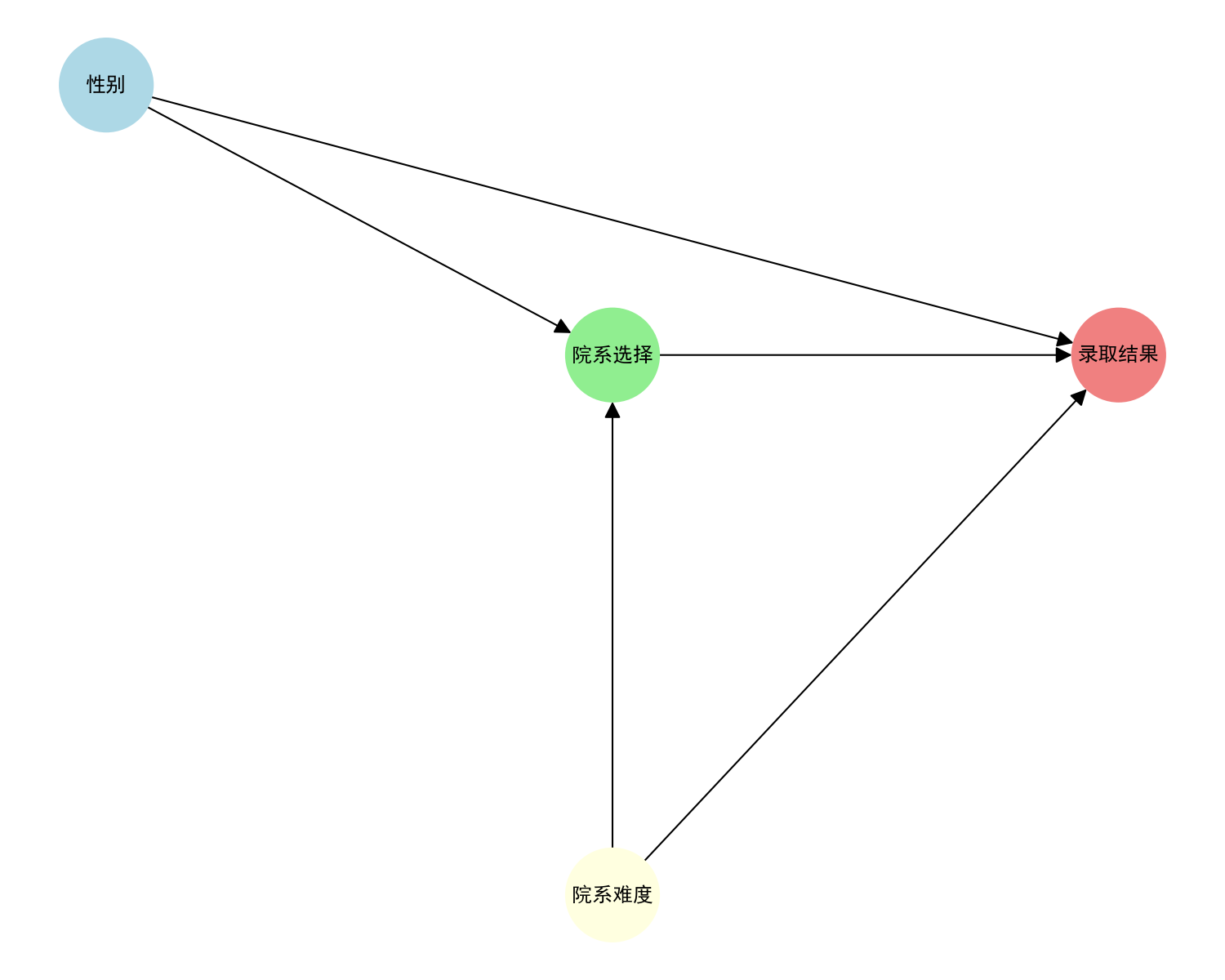

钥匙1:因果图------绘制变量间的"影响地图"

因果图是用图形表示变量间因果关系的工具。它不只是一张图,更是思考框架。

python

# 模拟辛普森悖论的因果图

import networkx as nx

import matplotlib.pyplot as plt

import matplotlib

# 配置中文字体(根据您的系统选择合适的方法)

# 方法1:使用系统自带的中文字体(Windows系统)

plt.rcParams['font.sans-serif'] = ['SimHei'] # 用来正常显示中文标签

plt.rcParams['axes.unicode_minus'] = False # 用来正常显示负号

# 创建因果图

G = nx.DiGraph()

G.add_edges_from([

("性别", "院系选择"), # 性别影响院系选择

("性别", "录取结果"), # 可能存在直接歧视

("院系选择", "录取结果"), # 院系选择影响录取

("院系难度", "录取结果"), # 院系固有难度

("院系难度", "院系选择"), # 难度影响选择

])

# 可视化

plt.figure(figsize=(10, 8))

pos = {

"性别": (0, 1),

"院系选择": (1, 0.5),

"录取结果": (2, 0.5),

"院系难度": (1, -0.5)

}

nx.draw(G, pos, with_labels=True, node_size=3000,

node_color=['lightblue', 'lightgreen', 'lightcoral', 'lightyellow'],

font_size=12, font_weight='bold', arrowsize=20)

plt.title("辛普森悖论的因果图表示", fontsize=16)

plt.show()

这张图告诉我们:要评估性别对录取的直接影响,必须控制"院系选择"这个中介变量。这就是因果推断的核心思想。

钥匙2:do-calculus------干预与观察的数学语言

2000年图灵奖得主Judea Pearl提出了do-calculus,它回答了这个问题:"如果强制改变某个变量,其他变量会如何变化?"

-

观察:P(录取|性别=女) = 看数据中女性的录取率

-

干预:P(录取|do(性别=女)) = 假设强制所有人都申请同样的院系,再看录取率

两者的区别就是选择偏差。do-calculus提供了从观察数据估计干预效果的数学工具。

钥匙3:双重机器学习------大数据时代的因果推断引擎

当变量很多时(高维问题),传统因果推断方法失效。Chernozhukov等人提出的双重机器学习,巧妙地将机器学习模型作为预测工具,用于估计因果效应。

python

import numpy as np

from sklearn.ensemble import RandomForestRegressor

from sklearn.model_selection import cross_val_predict

# 模拟数据:治疗T对结果Y的影响,受混淆变量X影响

np.random.seed(42)

n = 1000

X = np.random.normal(size=(n, 5)) # 5个混淆变量

T = 0.3*X[:,0] + 0.5*X[:,1] + np.random.normal(0, 0.5, n) # 治疗分配

Y = 0.8*T + 0.4*X[:,0] + 0.6*X[:,2] + np.random.normal(0, 0.3, n) # 结果

# 双重机器学习估计因果效应

def double_ml(X, T, Y):

# 第一步:用X预测T和Y的残差

model_T = RandomForestRegressor()

model_Y = RandomForestRegressor()

T_residual = T - cross_val_predict(model_T, X, T, cv=5)

Y_residual = Y - cross_val_predict(model_Y, X, Y, cv=5)

# 第二步:用T残差预测Y残差

effect = np.dot(T_residual, Y_residual) / np.dot(T_residual, T_residual)

return effect

true_effect = 0.8

estimated_effect = double_ml(X, T, Y)

print(f"真实因果效应: {true_effect:.3f}")

print(f"双重机器学习估计: {estimated_effect:.3f}")

print(f"绝对误差: {abs(true_effect-estimated_effect):.3f}")

因果机器学习的实战:Uplift建模

在营销中,我们想知道:给用户发优惠券,到底能增加多少购买概率?

传统方法:对比发券组和未发券组的购买率。

问题:发券组本来购买意愿就高(选择偏差)。

Uplift建模:估计每个用户的个体处理效应。

-

对于本来就要买的用户:发券是浪费

-

对于不发就不买的用户:发券才有效

python

# 简化的Uplift建模示例

import numpy as np # 添加这行导入语句

import pandas as pd

from sklearn.model_selection import train_test_split

from sklearn.ensemble import RandomForestClassifier

# 模拟用户数据

np.random.seed(42)

n_users = 2000

user_features = np.random.normal(size=(n_users, 10))

# 模拟潜在结果:Y0(不发券), Y1(发券)

Y0 = (0.3*user_features[:,0] + 0.5*user_features[:,1] +

np.random.normal(0, 0.2, n_users) > 0).astype(int)

Y1 = (0.8 + 0.3*user_features[:,0] + 0.5*user_features[:,1] +

np.random.normal(0, 0.2, n_users) > 0).astype(int)

# 模拟发券策略(基于部分特征)

T = (0.4*user_features[:,0] + 0.6*user_features[:,2] +

np.random.normal(0, 0.3, n_users) > 0).astype(int)

# 观测结果(只能看到一种情况)

Y_obs = np.where(T==1, Y1, Y0)

# 传统模型:预测发券后的购买概率

df = pd.DataFrame(user_features, columns=[f'X{i}' for i in range(10)])

df['T'] = T

df['Y'] = Y_obs

X_train, X_test, T_train, T_test, Y_train, Y_test = train_test_split(

user_features, T, Y_obs, test_size=0.2, random_state=42)

# 传统模型

model_traditional = RandomForestClassifier()

model_traditional.fit(X_train, Y_train)

acc_traditional = model_traditional.score(X_test, Y_test)

# Uplift模型:分别预测发券和不发券的情况

X_treat = X_train[T_train==1]

Y_treat = Y_train[T_train==1]

X_control = X_train[T_train==0]

Y_control = Y_train[T_train==0]

model_treat = RandomForestClassifier()

model_control = RandomForestClassifier()

model_treat.fit(X_treat, Y_treat)

model_control.fit(X_control, Y_control)

# 估计Uplift

uplift_test = (model_treat.predict_proba(X_test)[:,1] -

model_control.predict_proba(X_test)[:,1])

print(f"传统模型准确率: {acc_traditional:.3f}")

print(f"Uplift模型估计的个体处理效应范围: [{uplift_test.min():.3f}, {uplift_test.max():.3f}]")

print(f"高Uplift用户比例(>0.3): {(uplift_test > 0.3).mean():.1%}")

Uplift建模的价值:假设优惠券成本1元,转化利润10元。传统方法可能浪费大量预算在本来就会购买的用户身上,而Uplift建模可以精准定位那些"不发券不买,发券才买"的用户,将营销ROI提升2-5倍。

第二部分:可解释AI前沿------超越SHAP和LIME的"黑盒破解术"

SHAP和LIME的"中年危机"

SHAP(SHapley Additive exPlanations)和LIME(Local Interpretable Model-agnostic Explanations)无疑是可解释AI领域的明星。但它们正面临三大挑战:

-

局部性陷阱:每个预测单独解释,无法形成全局认知

-

特征工程依赖:解释的是特征重要性,而非人类可理解的概念

-

稳定性问题:相似的输入可能得到完全不同的解释

一个医疗诊断的典型案例:

python

# 假设我们有一个AI诊断肺炎的模型

# 使用SHAP解释为什么某张X光片被诊断为肺炎

import shap

# 模拟模型预测和SHAP解释

def explain_with_shap(model, image):

# SHAP会告诉你哪些像素重要

explainer = shap.DeepExplainer(model, background_images)

shap_values = explainer.shap_values(image)

# 结果显示:右下肺叶的几个像素最重要

# 但医生想问:为什么是这些像素?代表什么病理特征?

return shap_values医生真正关心的是:AI发现了什么医学特征?是毛玻璃影、实变还是胸腔积液? 但SHAP只能回答:这些像素比较重要。

概念解释:让AI用人类的语言思考

概念解释的核心思想:不是解释特征重要性,而是解释模型学习了哪些人类可理解的概念。

Google Research提出的**TCAV(Testing with Concept Activation Vectors)**方法:

-

定义概念:如"条纹""圆形""毛玻璃影"

-

找到概念在模型内部表示的方向(概念激活向量)

-

测试模型预测对这个概念的敏感性

python

# TCAV的简化思想演示

import numpy as np

# 假设模型内部有128维的表示

def model_internal_representation(image):

# 实际中这是深度学习模型的某一层

return np.random.normal(0, 1, 128)

# 定义"毛玻璃影"概念

def get_concept_vector(concept_name):

# 实际中需要用有概念标注的数据训练

concepts = {

"毛玻璃影": np.array([0.8, -0.2, 0.3, ...]), # 128维

"实变": np.array([0.1, 0.9, -0.1, ...]),

"胸腔积液": np.array([-0.3, 0.2, 0.7, ...]),

}

return concepts.get(concept_name, np.zeros(128))

# 计算概念敏感度

def concept_sensitivity(model_output, concept_vector):

# 计算模型输出变化对概念方向的导数

gradient = np.gradient(model_output, axis=0) # 简化表示

sensitivity = np.dot(gradient, concept_vector)

return sensitivity

# 使用示例

image_rep = model_internal_representation(x_ray_image)

concept = get_concept_vector("毛玻璃影")

sensitivity = concept_sensitivity(pneumonia_probability, concept)

print(f"模型诊断对'毛玻璃影'概念的敏感度: {sensitivity:.3f}")反事实解释:如果改变X,Y会怎样?

反事实解释回答的是:要达到不同的结果,输入应该如何最小程度地改变?

这在金融风控中特别有用:

-

用户问:"为什么我的贷款被拒?"

-

传统回答:"你的信用评分低,收入不足..."

-

反事实回答:"如果你年收入增加5万元,或信用卡债务减少2万元,贷款就会被批准。"

python

# 反事实解释的简化实现

import numpy as np

from sklearn.ensemble import RandomForestClassifier

from scipy.optimize import minimize

class CounterfactualExplainer:

def __init__(self, model, feature_names, categorical_indices=[]):

self.model = model

self.feature_names = feature_names

self.categorical_indices = categorical_indices

def generate_counterfactual(self, x_original, desired_class,

feature_weights=None, max_changes=3):

"""生成反事实解释"""

n_features = len(x_original)

if feature_weights is None:

feature_weights = np.ones(n_features)

def objective(x_candidate):

# 距离成本

distance_cost = np.sum(feature_weights * (x_candidate - x_original)**2)

# 预测差异成本

prob_original = self.model.predict_proba([x_original])[0]

prob_candidate = self.model.predict_proba([x_candidate])[0]

prediction_cost = (prob_original[desired_class] -

prob_candidate[desired_class])**2

# 稀疏性约束(限制改变的feature数量)

changes = (np.abs(x_candidate - x_original) > 1e-3)

sparsity_cost = max(0, changes.sum() - max_changes)**2

return distance_cost + 10*prediction_cost + 5*sparsity_cost

# 优化

result = minimize(objective, x_original.copy(),

bounds=[(0, 1) for _ in range(n_features)])

return result.x

# 使用示例

np.random.seed(42)

n_samples = 1000

n_features = 10

X = np.random.rand(n_samples, n_features)

y = (X[:,0] + 0.5*X[:,1] - 0.3*X[:,2] > 0.5).astype(int)

model = RandomForestClassifier()

model.fit(X, y)

explainer = CounterfactualExplainer(model, feature_names=[f"F{i}" for i in range(n_features)])

# 用户被拒绝贷款(类别0)

user_features = np.random.rand(n_features)

prediction = model.predict([user_features])[0]

if prediction == 0: # 被拒绝

# 生成如何获得批准(类别1)的反事实

counterfactual = explainer.generate_counterfactual(

user_features, desired_class=1, max_changes=3)

print("当前特征值:", user_features[:5])

print("反事实特征值:", counterfactual[:5])

print("需要改变的特征:")

for i in range(n_features):

if abs(counterfactual[i] - user_features[i]) > 0.1: # 显著改变

print(f" {explainer.feature_names[i]}: {user_features[i]:.2f} -> {counterfactual[i]:.2f}")临床决策支持的真实案例

梅奥诊所与MIT合作开发的可解释AI系统,用于败血症早期预警:

-

传统AI系统:提前4小时预测败血症风险,准确率85%

-

问题:医生不信任,因为不知道AI的推理过程

-

解决方案:加入概念解释

-

显示哪些生理指标异常(心率、血压、乳酸水平)

-

展示类似历史病例

-

提供反事实分析:"如果乳酸水平降低,风险会如何变化"

-

结果:医生采纳率从30%提升到90%,每年多挽救数百条生命。

第三部分:AI for Science------当机器学习遇见自然法则

AlphaFold2:蛋白质结构预测的"登月时刻"

2020年,DeepMind的AlphaFold2在蛋白质结构预测竞赛CASP14中取得惊人成绩,平均误差约1.6Å(原子直径级别)。这不仅解决了生物学50年来的重大挑战,更展示了AI+科学的无限可能。

AlphaFold2的核心创新:

-

注意力机制的多序列对齐:从进化信息中提取结构线索

-

几何约束的端到端训练:直接预测原子坐标的3D结构

-

物理知识嵌入:结合化学键长、键角等先验知识

python

# 简化的蛋白质结构预测思想

import numpy as np

def alphafold_simplified_idea(protein_sequence):

"""极度简化的AlphaFold思想演示"""

# 1. 进化信息提取

evolutionary_info = extract_evolutionary_info(protein_sequence)

# 2. 多序列对齐(注意力机制)

attention_weights = multi_sequence_attention(protein_sequence, evolutionary_info)

# 3. 几何表示学习

geometric_features = learn_geometric_representation(attention_weights)

# 4. 物理约束优化

structure = optimize_with_physical_constraints(geometric_features)

return structure

# AlphaFold2的核心:从序列到结构的端到端学习

def e2e_protein_folding(sequence):

"""端到端蛋白质折叠的简化演示"""

# 实际AlphaFold2有复杂的transformer架构

# 这里只展示思想

# 编码器:提取特征

residue_features = transformer_encoder(sequence)

# 结构模块:预测3D坐标

# 使用SE(3)等变网络,保证旋转平移不变性

coordinates = structure_module(residue_features)

# 迭代优化

for _ in range(3): # AlphaFold2有3次迭代

confidence_scores = confidence_module(coordinates, residue_features)

coordinates = refinement_module(coordinates, residue_features, confidence_scores)

return coordinates, confidence_scoresAlphaFold2的影响远不止蛋白质:

-

药物发现:快速筛选靶点

-

疾病研究:理解突变如何影响结构

-

合成生物学:设计全新蛋白质

气候建模:从物理方程到数据驱动的融合

传统气候模型基于物理方程,计算代价高昂。AI气候模型通过学习观测数据,可以快几个数量级地预测气候变化。

python

# 气候建模的AI方法演示

import numpy as np

from sklearn.ensemble import RandomForestRegressor

from sklearn.neural_network import MLPRegressor

class HybridClimateModel:

"""混合气候模型:结合物理知识和机器学习"""

def __init__(self, physical_constraints=True):

self.physical_constraints = physical_constraints

def train(self, historical_data, future_scenarios):

"""训练混合模型"""

# 历史数据:温度、CO2浓度、太阳辐射等

X_train, y_train = self.preprocess_data(historical_data)

if self.physical_constraints:

# 加入物理约束的机器学习

self.model = self.physically_constrained_ml(X_train, y_train)

else:

# 纯数据驱动

self.model = MLPRegressor(hidden_layer_sizes=(100, 50))

self.model.fit(X_train, y_train)

def physically_constrained_ml(self, X, y):

"""物理约束的机器学习"""

# 1. 能量守恒约束

def energy_constraint(predictions):

# 简化:全球能量平衡

return np.abs(predictions.sum() - X[:,0].sum()) # 粗略约束

# 2. 使用可解释模型

model = RandomForestRegressor(n_estimators=100)

model.fit(X, y)

# 3. 后处理调整以满足物理约束

return model

def predict(self, current_conditions, years_ahead):

"""预测未来气候"""

predictions = []

current = current_conditions

for year in range(years_ahead):

# 使用模型预测下一步

next_step = self.model.predict([current])[0]

# 应用物理约束修正

if self.physical_constraints:

next_step = self.apply_physical_constraints(current, next_step)

predictions.append(next_step)

current = next_step # 自回归预测

return np.array(predictions)AI气候模型的优势:

-

速度:传统模型需要超级计算机运行数周,AI模型只需几小时

-

不确定性量化:可以估计预测的置信区间

-

极端事件预测:更好地预测热浪、洪水等极端天气

材料发现:加速新材料研发10倍

传统材料研发靠"试错",发现一种新材料平均需要10-20年。AI可以将这个过程缩短到1-2年。

python

# 材料发现的AI工作流

class MaterialsDiscoveryAI:

def __init__(self):

self.property_predictor = None

self.generator = None

def workflow(self):

"""AI材料发现的工作流"""

steps = {

"1. 数据收集": "从文献、实验中收集材料数据",

"2. 特征工程": "提取晶体结构、化学成分等特征",

"3. 性质预测": "用机器学习预测材料的导电性、强度等",

"4. 生成设计": "用生成模型设计新材料结构",

"5. 实验验证": "合成最有前途的候选材料",

"6. 反馈循环": "用实验结果改进AI模型"

}

return steps

def discover_superconductor(self, target_temperature=150): # 150K超导体

"""发现高温超导体的简化演示"""

# 1. 搜索材料空间

candidate_materials = self.search_material_space(

elements=["Cu", "Ba", "Y", "O"], # 类似YBCO的元素

structure_types=["perovskite", "layered"]

)

# 2. 预测超导温度

predictions = []

for material in candidate_materials:

tc_pred = self.predict_tc(material) # 预测临界温度

confidence = self.prediction_confidence(material)

predictions.append((material, tc_pred, confidence))

# 3. 选择最有希望的候选

predictions.sort(key=lambda x: x[1], reverse=True)

best_candidates = predictions[:10] # 前10个

# 4. 考虑合成可行性

feasible_candidates = self.filter_by_synthesis_feasibility(best_candidates)

return feasible_candidates实际成果:伯克利实验室的"材料项目"已发现数千种有前途的新材料,其中几十种已实验验证。

第四部分:决策智能------当优化遇见机器学习

传统运筹学的局限

运筹学研究优化问题:资源分配、路径规划、库存管理。但它有两大局限:

-

精确模型依赖:需要精确知道所有参数

-

静态优化:一旦环境变化,解可能不再最优

强化学习+运筹学:自适应优化

强化学习通过试错学习最优策略,正好弥补运筹学的不足。

动态定价案例:航空公司如何实时调整票价?

python

import numpy as np

import matplotlib

import matplotlib.pyplot as plt

# 配置中文字体(根据您的系统选择合适的方法)

# 方法1:使用系统自带的中文字体(Windows系统)

plt.rcParams['font.sans-serif'] = ['SimHei'] # 用来正常显示中文标签

plt.rcParams['axes.unicode_minus'] = False # 用来正常显示负号

class DynamicPricingAgent:

"""动态定价智能体"""

def __init__(self, n_price_levels=10):

self.n_price_levels = n_price_levels

self.demand_bins = 5

self.competition_bins = 5

self.n_states = self.demand_bins * self.competition_bins

# 修正:Q表应该是状态数×动作数

self.q_table = np.zeros((self.n_states, n_price_levels))

self.learning_rate = 0.1

self.discount_factor = 0.9

self.epsilon = 0.1 # 探索率

def state_representation(self, market_conditions):

"""将市场状况编码为状态"""

# 简化:基于需求水平和竞争价格

demand_level = self.discretize(market_conditions['demand'], self.demand_bins)

competition_price = self.discretize(market_conditions['competition_price'], self.competition_bins)

return (demand_level, competition_price)

def discretize(self, value, n_bins):

"""连续值离散化"""

# 确保值在[0, 1]范围内

value = max(0, min(1, value))

return min(int(value * n_bins), n_bins - 1)

def state_to_index(self, state):

"""将二维状态转换为一维索引"""

demand_idx, competition_idx = state

return demand_idx * self.competition_bins + competition_idx

def choose_price(self, state, current_price):

"""选择价格动作"""

if np.random.random() < self.epsilon:

# 探索:随机选择价格

return np.random.randint(0, self.n_price_levels)

else:

# 利用:选择Q值最高的价格

state_idx = self.state_to_index(state)

return np.argmax(self.q_table[state_idx])

def update(self, state, action, reward, next_state):

"""更新Q表"""

state_idx = self.state_to_index(state)

next_state_idx = self.state_to_index(next_state)

# Q-learning更新公式

current_q = self.q_table[state_idx, action]

max_future_q = np.max(self.q_table[next_state_idx])

new_q = current_q + self.learning_rate * (

reward + self.discount_factor * max_future_q - current_q

)

self.q_table[state_idx, action] = new_q

def simulate_market(self, days=100):

"""模拟市场环境"""

prices = []

revenues = []

# 初始状态:中等需求和中等竞争价格

current_state = (2, 2)

current_price_idx = 5 # 中间价格

for day in range(days):

# 市场条件变化

market_conditions = {

'demand': np.clip(np.random.normal(0.5, 0.1), 0, 1), # 限制在[0,1]

'competition_price': np.clip(np.random.normal(0.6, 0.15), 0, 1) # 限制在[0,1]

}

# 当前状态

state = self.state_representation(market_conditions)

# 选择价格动作

price_action = self.choose_price(state, current_price_idx)

# 价格索引转实际价格

price = 100 + price_action * 20 # 假设价格范围100-280

# 模拟需求响应(价格弹性)

base_demand = 100 * market_conditions['demand']

price_elasticity = -1.5

demand = base_demand * (price / 200) ** price_elasticity

# 收益

revenue = price * demand

# 奖励(考虑市场份额)

competition_price = market_conditions['competition_price'] * 200

competition_ratio = price / competition_price if competition_price > 0 else 2.0

if competition_ratio < 1.1: # 价格不超过竞争对手10%

market_share = 0.5

else:

market_share = 0.2

reward = revenue * market_share

# 下一状态

next_market_conditions = {

'demand': np.clip(

market_conditions['demand'] + np.random.normal(0, 0.05), 0, 1

),

'competition_price': np.clip(

market_conditions['competition_price'] + np.random.normal(0, 0.03), 0, 1

)

}

next_state = self.state_representation(next_market_conditions)

# 更新Q表

self.update(state, price_action, reward, next_state)

# 更新当前价格和状态

current_price_idx = price_action

current_state = state

prices.append(price)

revenues.append(revenue)

# 衰减探索率

self.epsilon *= 0.995

return prices, revenues

# 运行模拟

agent = DynamicPricingAgent()

prices, revenues = agent.simulate_market(days=200)

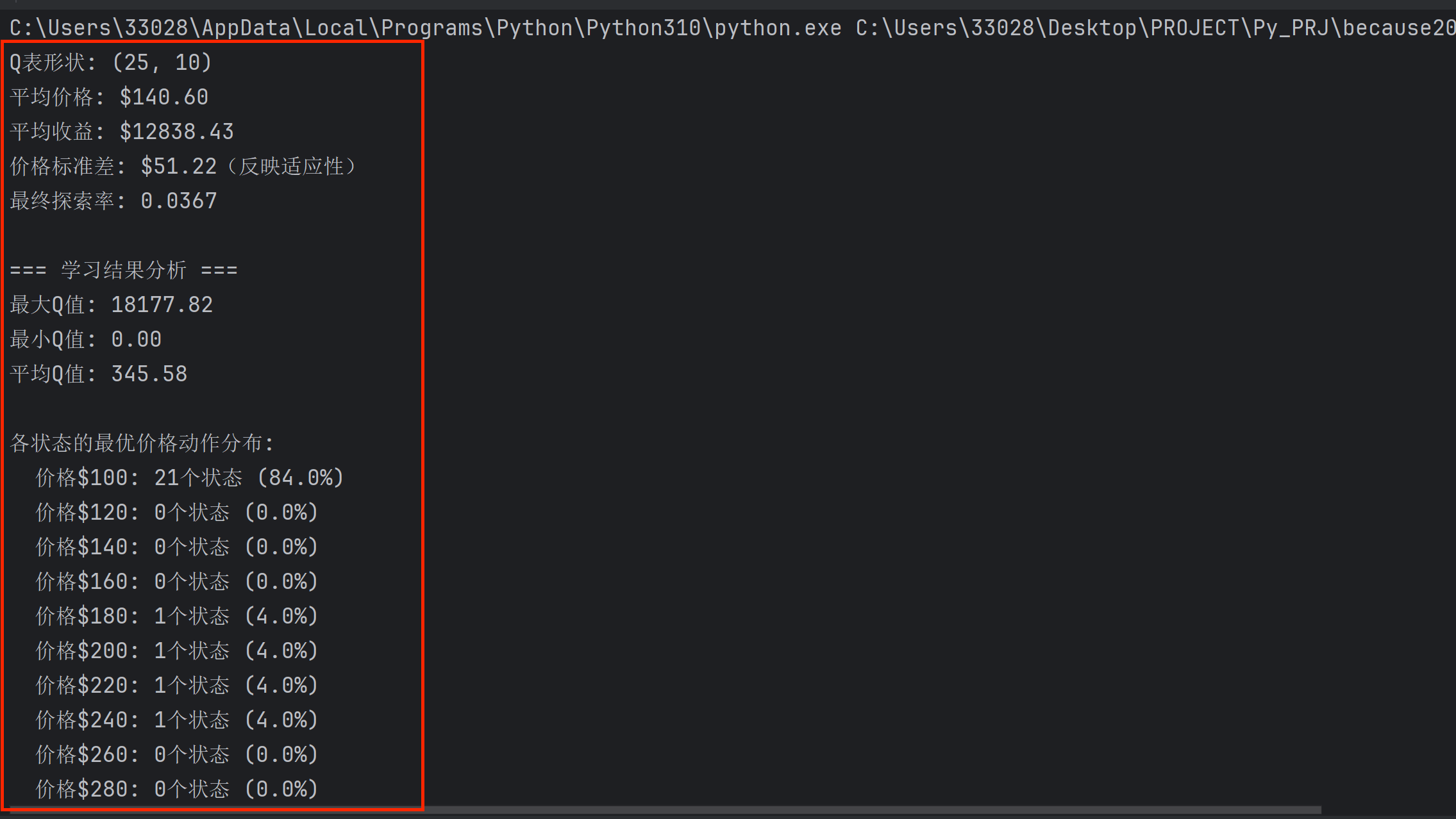

print(f"Q表形状: {agent.q_table.shape}")

print(f"平均价格: ${np.mean(prices):.2f}")

print(f"平均收益: ${np.mean(revenues):.2f}")

print(f"价格标准差: ${np.std(prices):.2f}(反映适应性)")

print(f"最终探索率: {agent.epsilon:.4f}")

# 可视化学习过程

import matplotlib.pyplot as plt

fig, axes = plt.subplots(2, 2, figsize=(12, 10))

# 价格随时间变化

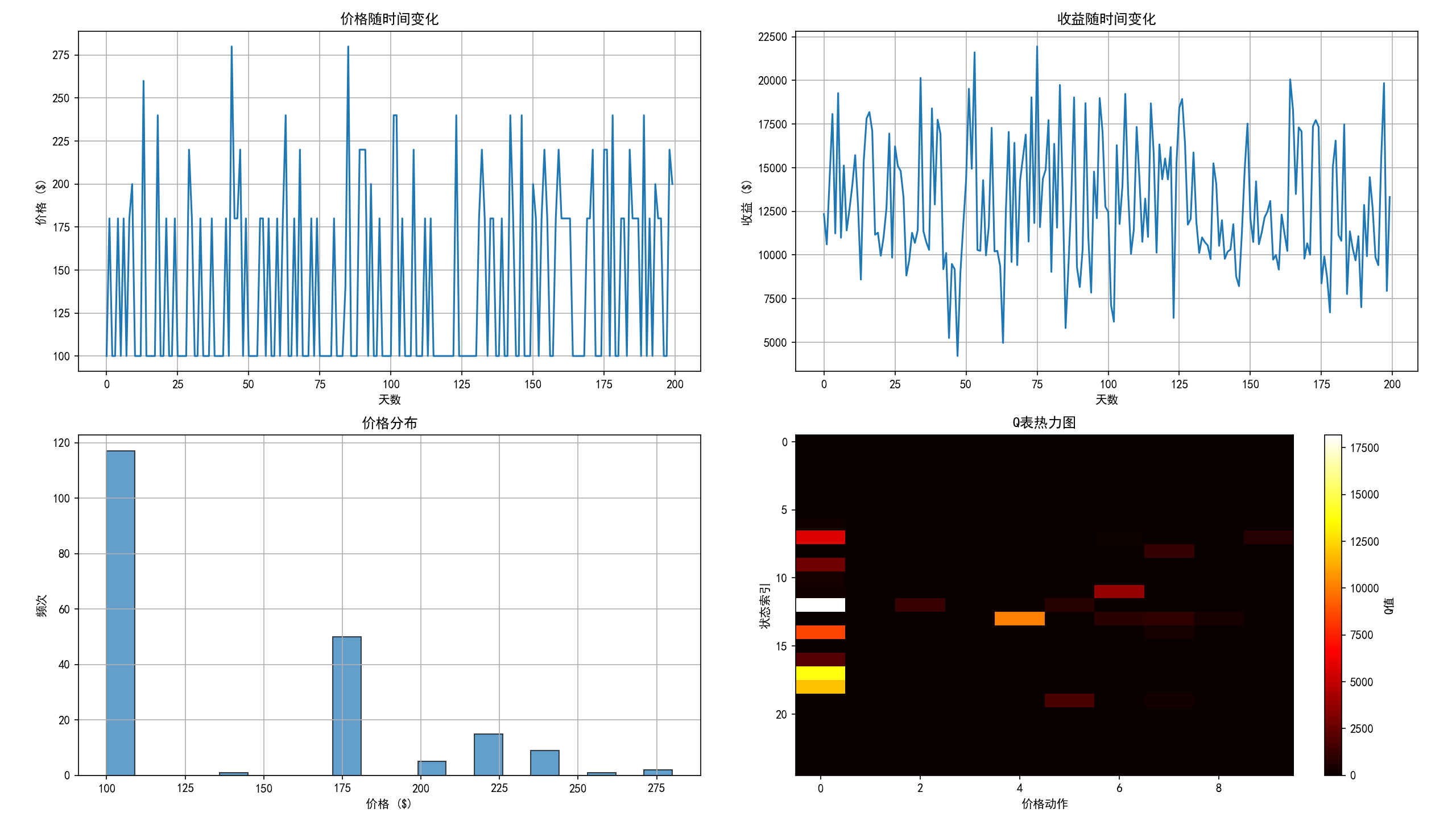

axes[0, 0].plot(prices)

axes[0, 0].set_xlabel('天数')

axes[0, 0].set_ylabel('价格 ($)')

axes[0, 0].set_title('价格随时间变化')

axes[0, 0].grid(True)

# 收益随时间变化

axes[0, 1].plot(revenues)

axes[0, 1].set_xlabel('天数')

axes[0, 1].set_ylabel('收益 ($)')

axes[0, 1].set_title('收益随时间变化')

axes[0, 1].grid(True)

# 价格分布直方图

axes[1, 0].hist(prices, bins=20, edgecolor='black', alpha=0.7)

axes[1, 0].set_xlabel('价格 ($)')

axes[1, 0].set_ylabel('频次')

axes[1, 0].set_title('价格分布')

axes[1, 0].grid(True)

# Q表热力图

im = axes[1, 1].imshow(agent.q_table, aspect='auto', cmap='hot')

axes[1, 1].set_xlabel('价格动作')

axes[1, 1].set_ylabel('状态索引')

axes[1, 1].set_title('Q表热力图')

plt.colorbar(im, ax=axes[1, 1], label='Q值')

plt.tight_layout()

plt.show()

# 分析学习结果

print("\n=== 学习结果分析 ===")

print(f"最大Q值: {np.max(agent.q_table):.2f}")

print(f"最小Q值: {np.min(agent.q_table):.2f}")

print(f"平均Q值: {np.mean(agent.q_table):.2f}")

# 找到最优策略

optimal_policy = np.argmax(agent.q_table, axis=1)

print(f"\n各状态的最优价格动作分布:")

for action in range(agent.n_price_levels):

count = np.sum(optimal_policy == action)

price = 100 + action * 20

print(f" 价格${price}: {count}个状态 ({count / len(optimal_policy):.1%})")

决策智能的实际应用:

-

物流优化:UPS的ORION系统结合运筹学和机器学习,每年节省1亿英里路程

-

能源管理:谷歌数据中心使用AI优化冷却,能效提升40%

-

金融投资:BlackRock的Aladdin平台管理21万亿美元资产

结语:从预测到理解,从优化到创造

我们走过了因果机器学习的严谨推理、可解释AI的透明决策、科学发现的跨界融合、决策智能的动态优化。这不仅仅是技术的演进,更是机器学习范式的根本转变。

三个关键转变

-

从相关性到因果性:不再满足于"是什么",而要追问"为什么"

-

从黑盒到玻璃盒:AI的决策过程需要透明、可解释、可信任

-

从数据驱动到知识融合:结合领域知识、物理定律、人类直觉