一、什么是逻辑回归?

逻辑回归(Logistic Regression)虽然名字带"回归",但本质是一个分类算法 ,尤其擅长解决二分类问题(也可扩展至多分类)。

核心思想

- 通过线性组合输入特征:

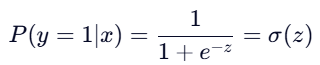

- 将 z 映射到 (0,1) 区间,表示属于正类的概率:

- 决策规则:若 P(y=1∣x)>0.5P(y=1∣x)>0.5 ,则预测为正类(1),否则为负类(0)。

优点 :模型简单、可解释性强(权重反映特征重要性)、训练高效。

局限:假设特征与对数几率(log-odds)线性相关,对非线性关系建模能力弱。

二、如何判断逻辑回归模型好不好?------ 关键评估指标

在不平衡数据中,准确率(Accuracy)是"毒药"!例如欺诈检测中,99.9% 的交易正常,模型全预测"正常"也能获得 99.9% 准确率,但毫无价值。

必看指标(基于混淆矩阵)

| 指标 | 意义 | 适用场景 |

|---|---|---|

| 召回率(Recall) | 查全率:有多少正样本被找出来了? | 欺诈检测、疾病筛查(宁可误报,不可漏报) |

| 精确率(Precision) | 查准率:预测为正的样本中有多少是真的? | 垃圾邮件过滤(避免误杀正常邮件) |

| F1-Score | 精确率与召回率的调和平均 | 综合评估 |

| AUC-ROC | 模型在不同阈值下的整体性能 | 通用,尤其适合不平衡数据 |

💡 银行老赖检测 :召回率是核心指标!目标是尽可能找出所有潜在老赖客户(即使误报一些正常交易)。

三、模型诊断:欠拟合 vs 过拟合

1. 欠拟合(Underfitting)

- 表现:训练集和测试集性能都很差(如 Recall < 0.5)

- 原因 :

- 特征太少或信息不足

- 正则化过强(C 值太小)

- 模型太简单(逻辑回归本身线性)

- 解决 :

- 增加特征(如多项式特征、交叉特征)

- 减小正则强度(增大

C参数) - 尝试更复杂模型(如随机森林)

2. 过拟合(Overfitting)

- 表现:训练集性能很好(Recall ≈ 1.0),但测试集性能差

- 原因 :

- 特征过多(尤其高维稀疏数据)

- 正则化不足(C 值太大)

- 训练数据太少

- 解决 :

- 增加正则化(减小

C,或使用 L1 正则) - 特征选择(L1 正则自动稀疏化)

- 增加训练数据(或使用过采样)

- 增加正则化(减小

🔍 诊断工具 :绘制学习曲线(Learning Curve),观察训练/验证分数随样本量的变化。

四、优化策略:提升召回率的关键技术

面对不平衡数据,单纯调参效果有限。必须结合采样技术 + 交叉验证。

1. 交叉验证

- 作用 :在训练阶段可靠评估模型泛化能力,指导超参数选择(如正则强度

C)。 - 陷阱 :若先对整个训练集采样再 CV,会导致数据泄露(每折验证集信息已用于生成合成样本)。

- 正确做法 :使用

imblearn.Pipeline,确保每折 CV 内部独立采样。

python

from imblearn.pipeline import Pipeline

from sklearn.model_selection import cross_val_score

pipeline = Pipeline([

('smote', SMOTE(random_state=42)), # 每折内过采样

('scaler', StandardScaler()),

('lr', LogisticRegression(C=1.0))

])

# 安全的交叉验证

cv_scores = cross_val_score(pipeline, X_train, y_train, cv=5, scoring='recall')2. 下采样

- 原理:随机删除部分多数类样本,使正负样本平衡。

- 优点:训练快,实现简单。

- 缺点 :丢失大量有用信息,可能导致模型对正常样本欠拟合。

- 适用:数据量极大,计算资源紧张。

python

from imblearn.under_sampling import RandomUnderSampler

undersampler = RandomUnderSampler(random_state=42)

X_res, y_res = undersampler.fit_resample(X_train, y_train)3. 过采样

- SMOTE(Synthetic Minority Oversampling Technique) :

- 在特征空间中,基于 K 近邻合成新少数类样本。

- 例如:在两个0样本之间插值生成新0样本。

- 优点:保留全部原始数据,提升召回率效果显著。

- 缺点:可能过拟合(尤其高维数据),训练时间增加。

- 适用:中小规模数据,关注少数类检测。

python

from imblearn.over_sampling import SMOTE

smote = SMOTE(random_state=42)

X_res, y_res = smote.fit_resample(X_train, y_train)重要原则 :

采样仅用于训练!测试集必须保持原始分布,否则评估结果无效。

五、完整实战流程(以银行卡用户是否是老赖检测为例)

python

import pandas as pd

from sklearn.model_selection import train_test_split, cross_val_score

from sklearn.linear_model import LogisticRegression

from sklearn.preprocessing import StandardScaler

from sklearn.metrics import recall_score, classification_report

from imblearn.over_sampling import SMOTE

from imblearn.pipeline import Pipeline

# 加载数据

data = pd.read_csv('creditcard.csv')

X = data.drop('Class', axis=1)

y = data['Class']

# 划分训练/测试集(测试集保持原始分布!)

X_train, X_test, y_train, y_test = train_test_split(

X, y, test_size=0.2, random_state=42, stratify=y

)

X_train['Class'] = y_train

data_train = X_train

"""下采样解决样本不均衡问题"""

positive_eg = data_train[data_train['Class'] == 0] # 获取到了所有标签 (class) 为0的数据

negative_eg = data_train[data_train['Class'] == 1] # 获取到了所有标签(class)为1的数据

positive_eg = positive_eg.sample(len(negative_eg)) # sample表示随机从参数里面选择数据.

# 拼接数据 random.sample(10) random.choice()区别:

data_c = pd.concat([positive_eg, negative_eg]) # 是把两个pandas数据组合为一个

data_c_x = data_c.drop('Class', axis=1)

data_c_y = data_c['Class']

# 定义 C 参数范围

c_param_range = [0.01, 0.1, 1, 10, 100]

scores = []

for c in c_param_range:

# 创建 Pipeline:先标准化,再逻辑回归

pipeline = Pipeline([

('scaler', StandardScaler()),

('lr', LogisticRegression(C=c, penalty='l2', solver='lbfgs', max_iter=1000))

])

# 交叉验证(自动在每折内做标准化,无数据泄露)

cv_scores = cross_val_score(pipeline, data_c_x, data_c_y, cv=8, scoring='recall')

score_mean = cv_scores.mean()

scores.append(score_mean)

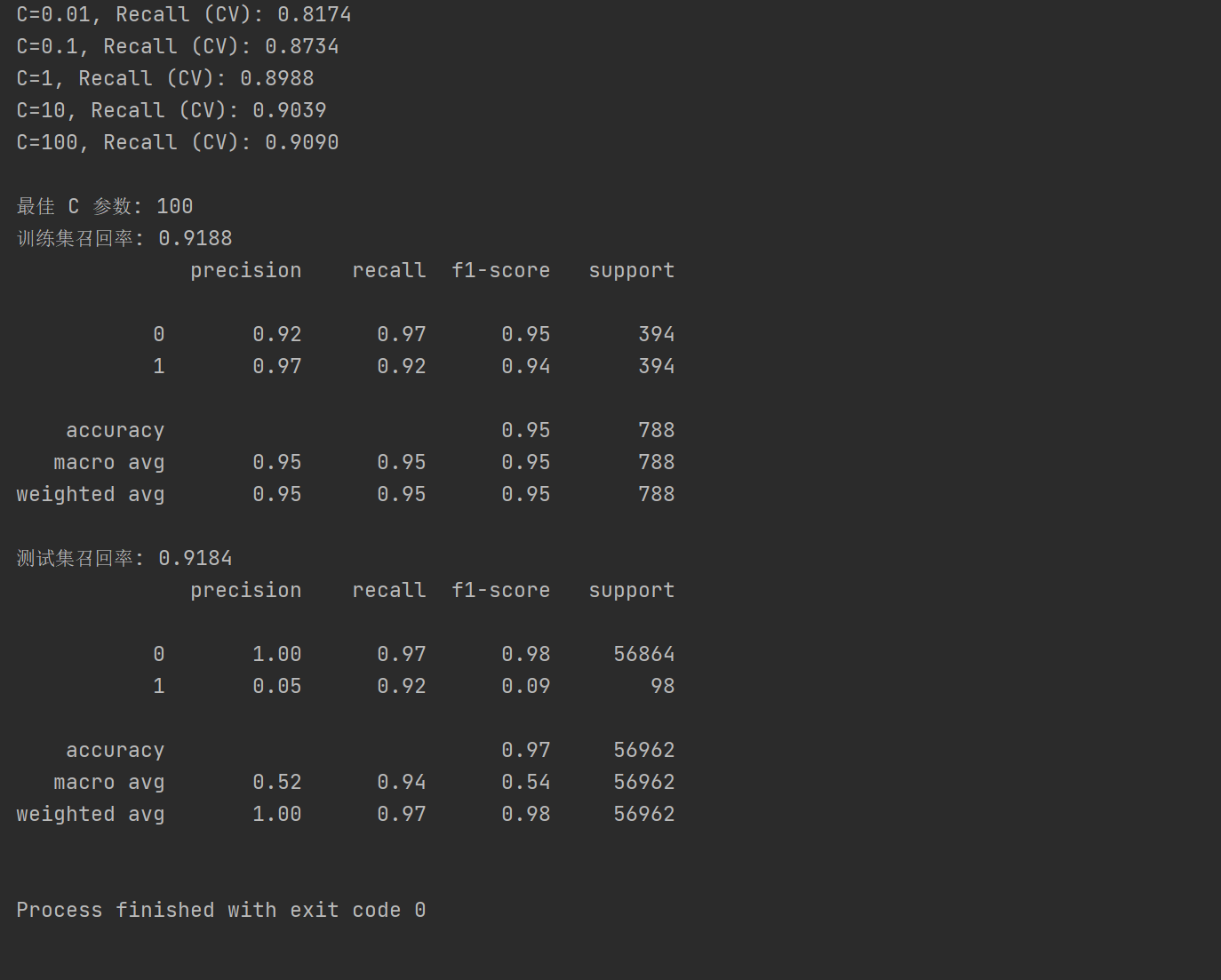

print(f"C={c}, Recall (CV): {score_mean:.4f}")

# 找到最佳 C

best_c = c_param_range[scores.index(max(scores))]

print(f"\n最佳 C 参数: {best_c}")

# 用最佳 C 训练最终模型

final_pipeline = Pipeline([

('scaler', StandardScaler()),

('lr', LogisticRegression(C=best_c, penalty='l2', solver='lbfgs', max_iter=1000))

])

# 模型训练

final_pipeline.fit(data_c_x, data_c_y)

# 训练集预测

data_c_pred = final_pipeline.predict(data_c_x)

train_recall = recall_score(data_c_y, data_c_pred)

print(f"训练集召回率: {train_recall:.4f}")

print(classification_report(data_c_y, data_c_pred))

# 测试集预测

y_pred = final_pipeline.predict(X_test)

test_recall = recall_score(y_test, y_pred)

print(f"测试集召回率: {test_recall:.4f}")

print(classification_report(y_test, y_pred))运行结果: